Salaried investors will find EPF liquidity is no longer such a heady matter. The 2026 Scheme lets you check what you can put your hands on online before you even put in a claim. But be aware of the new guardrails and TDS; they put a price on hasty departures.

What changed and why it matters

The 2026 overhauls have taken well over a dozen advance rules and put them in one of three buckets: for essentials, a home, or an exception. It is more than a tidy-up; for a saver in a bind, it means less time wondering and more time acting.

There is a framework to access now. Put in 12 months of service and up to 75% of the total is available. The other 25% is non-negotiable, set aside to see your retirement fund grow.

It is a way to have some liquid capital at hand without putting future savings at risk.

Tax friction: the key risk to returns

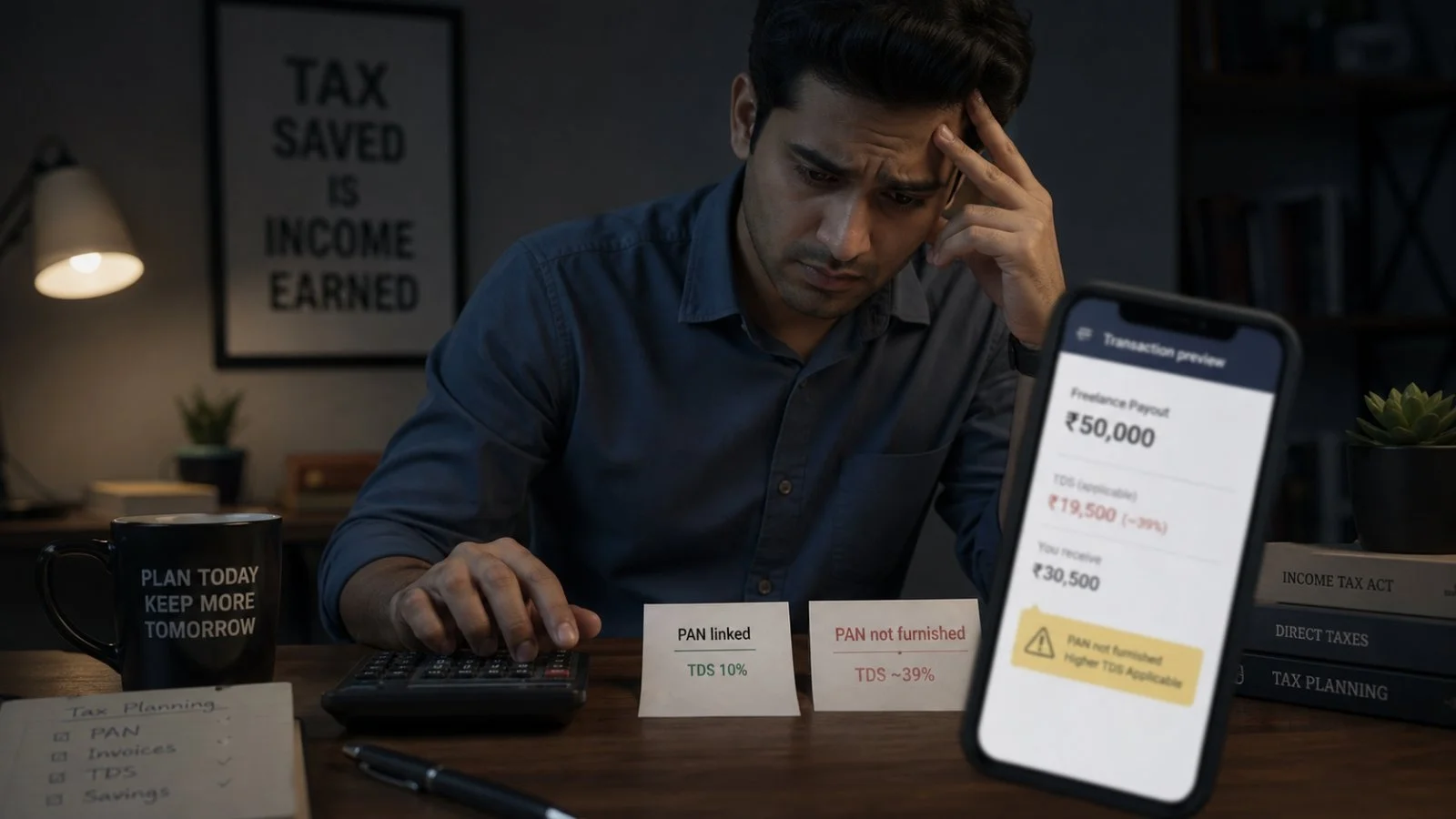

You may run into some tax drag with an early exit. Should you pull out before five years of unbroken service, TDS comes into play. It is a factor to keep in mind when you are working out cash flow.

Provided your PAN is on file with the EPF, any sum over Rs 50,000 will be taxed at 10%. Come in under that figure and there is no deduction, five-year mark or not.

Without a PAN, the TDS is levied at the top rate of 39. Then again, if you do not cross the taxable threshold, a Form 15G or 15H will do the trick to sidestep it.

A TDS is not the end of the story. If the actual tax is less, a refund is in order come filing season. For an investor, the point is to link the PAN, watch the five-year clock and let nothing go to waste.

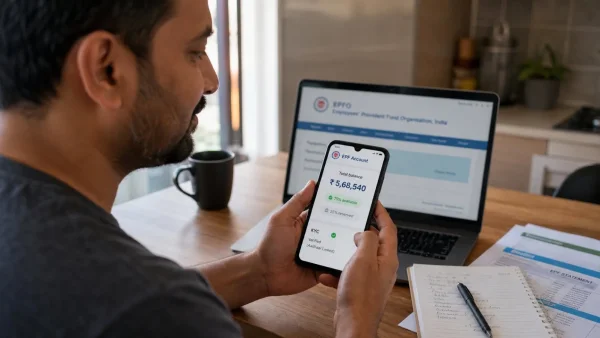

How to see your EPF withdrawal limit online

Head to the EPFO portal and you will be shown the maximum you can take, given your record and reason. It is a way to make sure a claim is not turned down on a technicality.

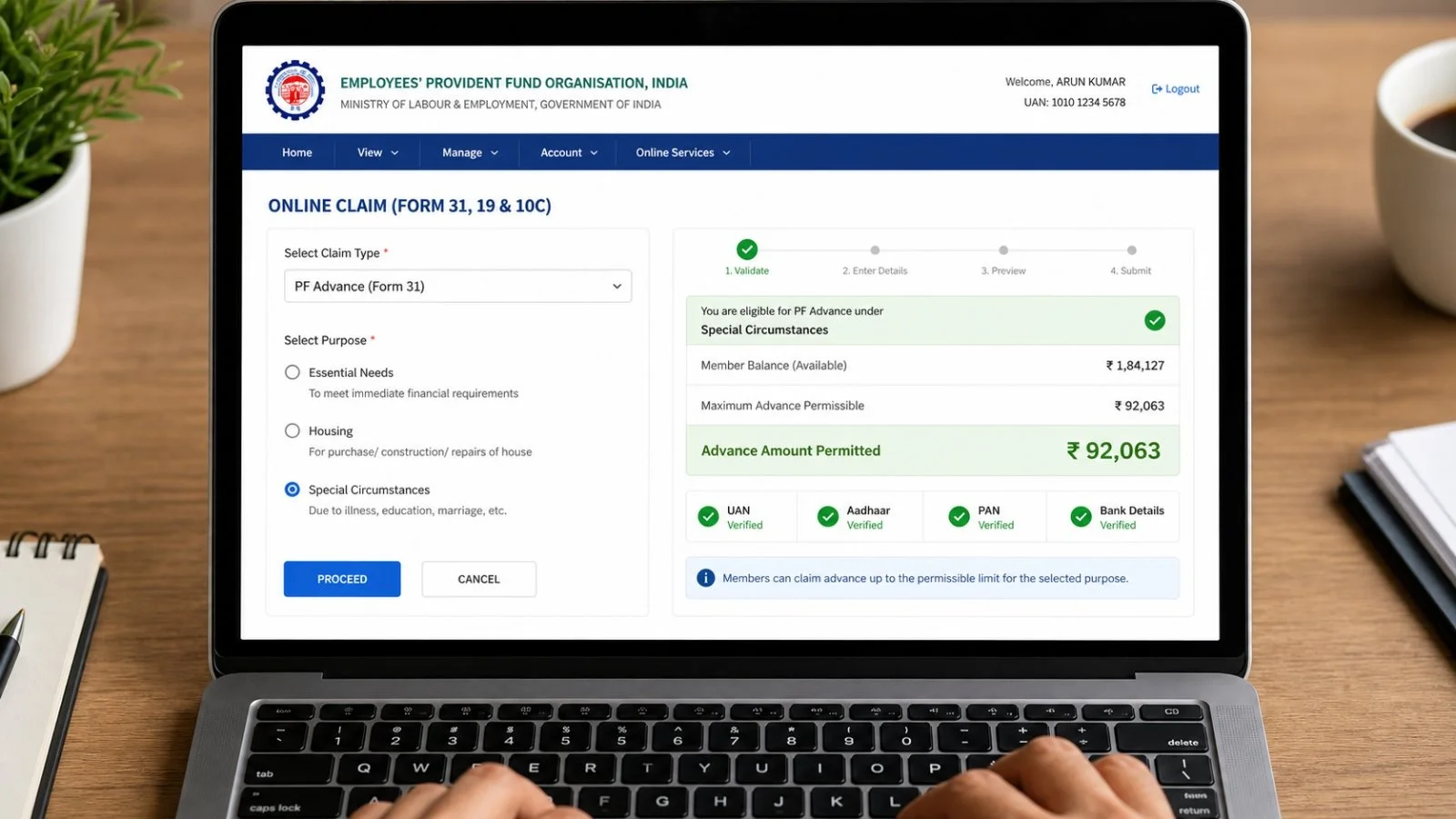

If a partial withdrawal is what is needed, the right move in the online system is to opt for PF Advance (Form 31) and not the Final Settlement (Form 19) or Pension Withdrawal (Form 10C). If you have older accounts that haven’t been put together, make sure to choose the right spell of service from your employer list.

From there, select the reason for the withdrawal-be it an essential need, housing or some other special case. The portal will put the allowable figure in front of you at once. It is a good idea to have your UAN, Aadhaar, PAN and bank information KYC-verified so as not to hold things up.

When can one make a full withdrawal?

The EPF is meant for retirement, and that is when a full payout is in order. There are exceptions, however: if a member has left an employer and is out of work, the rules allow for a complete withdrawal.

For more specific needs like putting a child through college, a wedding, medical bills, a home or a loan on one, partial withdrawals are open to members. How much can be taken out is a function of the purpose, the balance in the account and how long one has been in service.

Since the fine print is different for each category, the new way of classifying and showing what is eligible on screen is useful. It boils down the details to a number you can work with.

A few planning points for the investor

Any claim should be in step with one’s wider financial picture. With 25% of the fund now set aside for the long term, it is best to view the EPF as a source of last-resort liquidity to let compounding do its job.

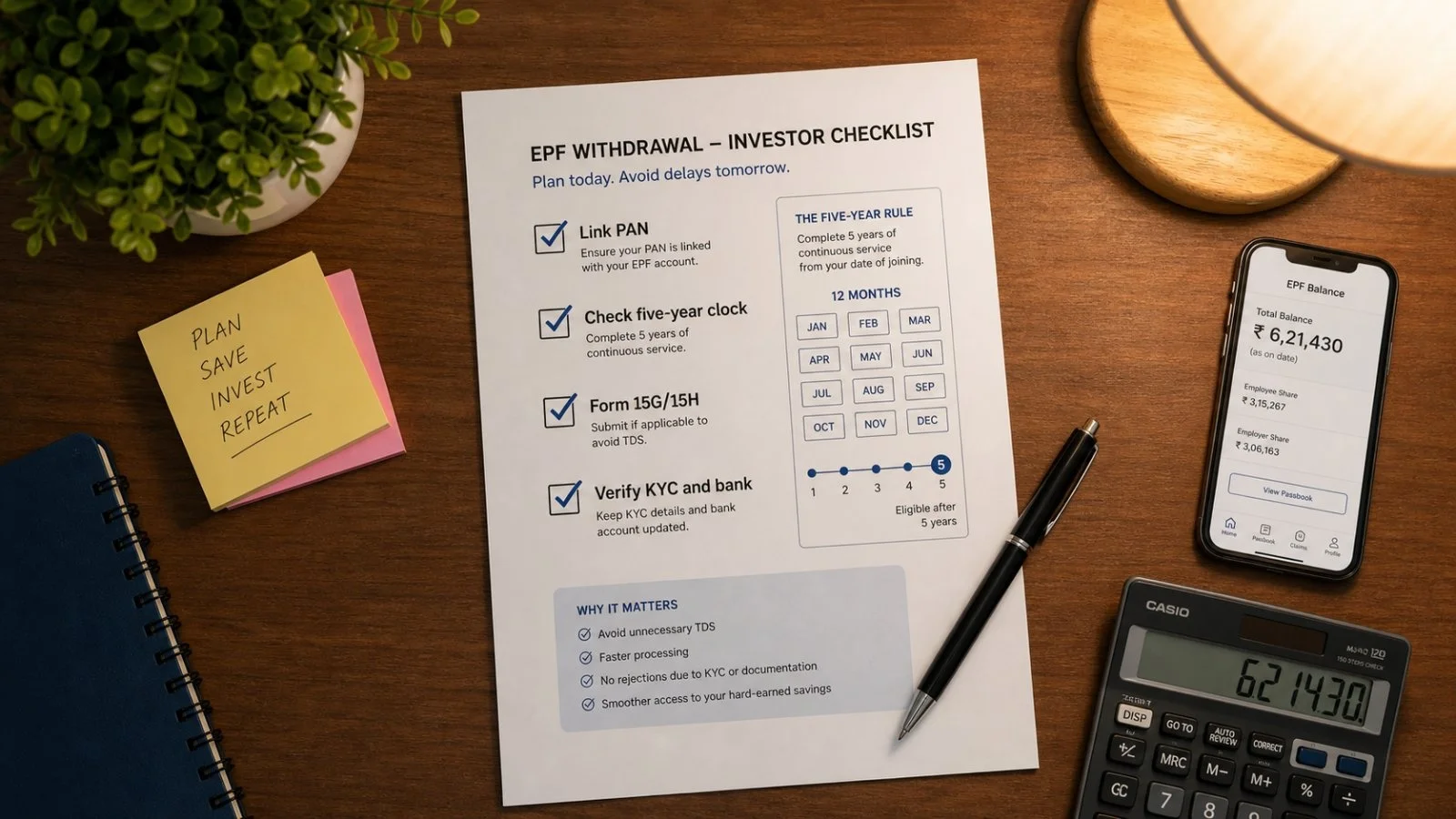

To keep things running without a hitch:

– Link the PAN; otherwise TDS is 39%

– See where one stands on the five-year mark

– Put in a 15G or 15H form if the case allows

– Make sure all KYC and employer data is in order

– File the right form on the site

*

More than a change in the rules

Having a clear view of what is available takes the guesswork out of an emergency. A borrower can turn to this lower-cost option instead of expensive credit. On the flip side, the 25% reserve puts a floor under what is saved for later. Those who were in the habit of making ad-hoc withdrawals may find themselves with a better sense of the trade-offs.

What to expect from here on

Processing should be less of a chore as the online system makes it easier to prove intent and eligibility. For those with a history of multiple employers, it will be on them to ensure their records and KYC are in shape, as the numbers are only as good as the data.

In effect, the new setup is designed to steer members toward withdrawals that are well thought out. Better for cash flow now and a stronger position down the line.

The short of it**

After a year in service, 75% of the EPF is accessible, but the rest is off-limits. An early out before the five-year point will see TDS applied: 10% with a linked PAN (for amounts over Rs 50,000) and 39% if not. The EPFO portal is the place to check the limit and make a move with no room for error.