Loads of employed Indians with a regular salary are potentially getting less money for retirement because of incorrect ideas about how EPF (Employee Provident Fund) interest, pensions, and retirement age work. For those saving for the future, the problem is pretty clear: a small misunderstanding can lead to taking money out too soon, missing out on the 8.25% interest it earns over time, and getting your pension later than you should. Here’s what really makes a difference to how much you’ll have.

Why this matters for your retirement plan

EPF is at the heart of most people’s retirement savings from a job. Employees put 12% of their basic salary in, and employers add 12% as well. Some of the employer’s part goes to EPS (Employees’ Pension Scheme) which provides a pension for life.

Currently, the fund gets 8.25% interest each year. You can claim tax relief on what you pay in under Section 80C, and you usually don’t pay tax on the money when you get it out, if you’ve been in the scheme for at least 5 years without a break. You are allowed to take some of the money out early for things like a house, medical bills, or school fees, but only if you’re eligible.

Interest does not vanish the day you stop working

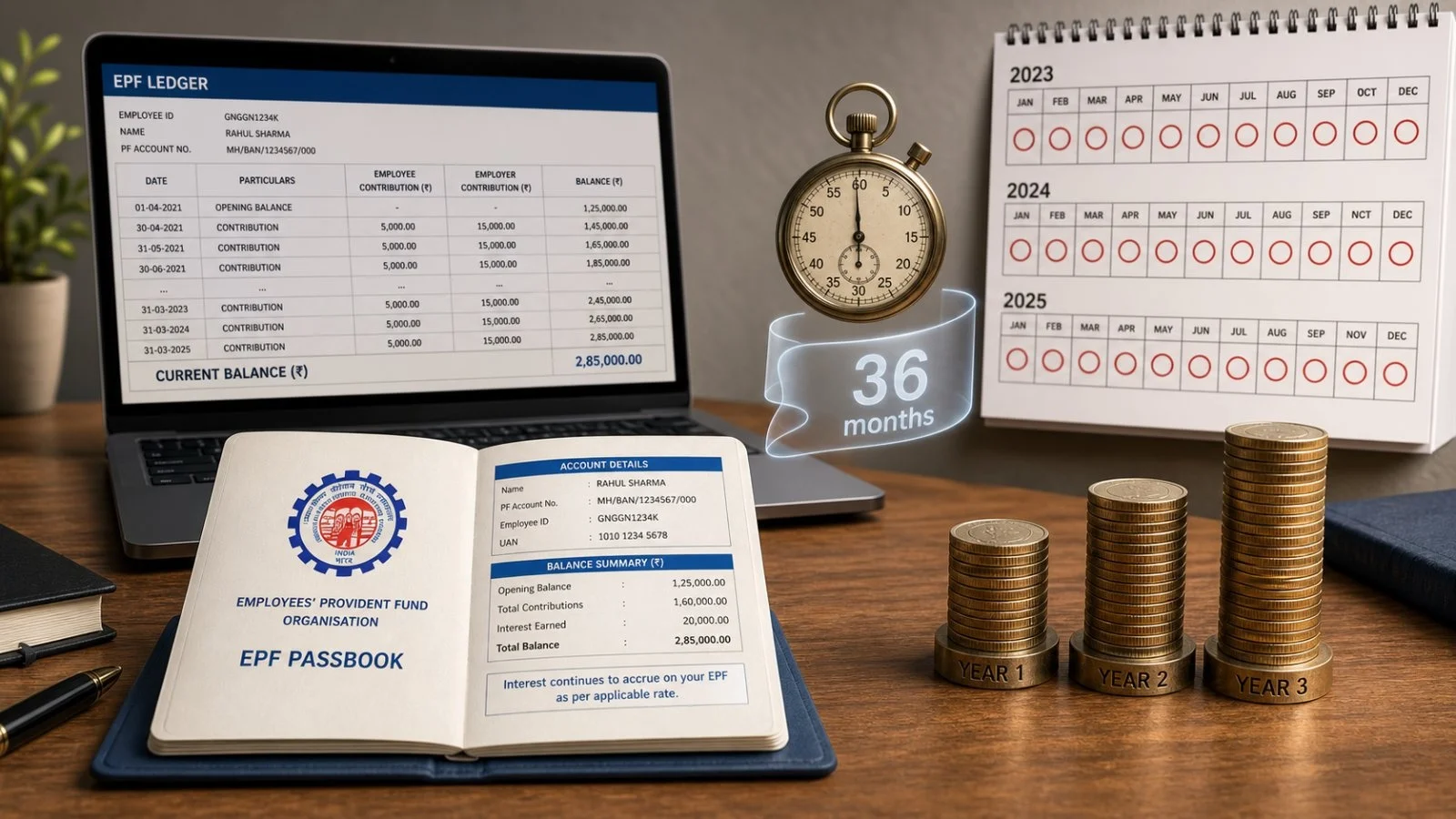

Lots of people wrongly think that the interest stops as soon as you leave a job and this is expensive. Your EPF money keeps earning interest for up to re years after your last payment. After that, if you don’t add anything to it, the account becomes inactive and stops gaining interest.

Importantly, whether you get interest depends on activity in the account, not your age. Taking time off work doesn’t automatically make your account inactive. It’s considered inactive after 36 months of no contributions. Even when it is inactive, you can still get at the money by transferring it or withdrawing it, as long as you follow the rules.

Here are the key interest and inactivity checkpoints investors should note:

– Interest accrues up to 3 years after last contribution

– Inactivity begins only after 36 months with no deposits

– Inoperative accounts remain accessible for transfer or withdrawal

Retirement age vs pension start: the real trigger

A lot of confusion is around when you retire. Many think EPF has a retirement age of 60. However, the more important age in the rules is 58, because that is when you can start getting benefits from the Employees’ Pension Scheme.

With EPS, you get a monthly payment for life from age 58, even if you’re still working. This payment depends on whether you meet the basic requirements. Periods when you haven’t been contributing aren’t included when calculating your pension, so when you change jobs, it’s important to have the correct start and end dates for your employment.

How EPS is calculated and the current floor

EPS is calculated with this formula: (Pensionable Salary x Pensionable Service) / 70. Pensionable service only counts the years where you actually paid into the scheme. The lowest monthly pension you can get is Rs 1,000 until March 2026. A parliamentary committee has suggested this should be Rs 7,500, but there’s been no official announcement as yet.

The cost of getting the rules wrong

Closing your account when you change jobs can stop the interest from growing and mean you no longer meet the 5-year rule for tax benefits. Thinking interest stops when you retire might mean you withdraw money too early, and lose up to 3 years of interest. Getting the pension start age wrong could mean you delay claiming money you could have had from age 58.

Think about the effect of compounding. At 8.25%, even a little longer of earning interest can noticeably increase your total savings. Combine that with tax benefits and the timing of your EPS, and the difference between planning based on what’s true and what people think is true is a lot over 20 to 30 years.

What investors should do now

Begin by making sure your plans are based on how the money really works with EPF and EPS. Interest is calculated on what’s paid in. You can get your pension from 58, if you’re eligible. It’s how active your account is that determines when the interest stops, not your birthday or job title.

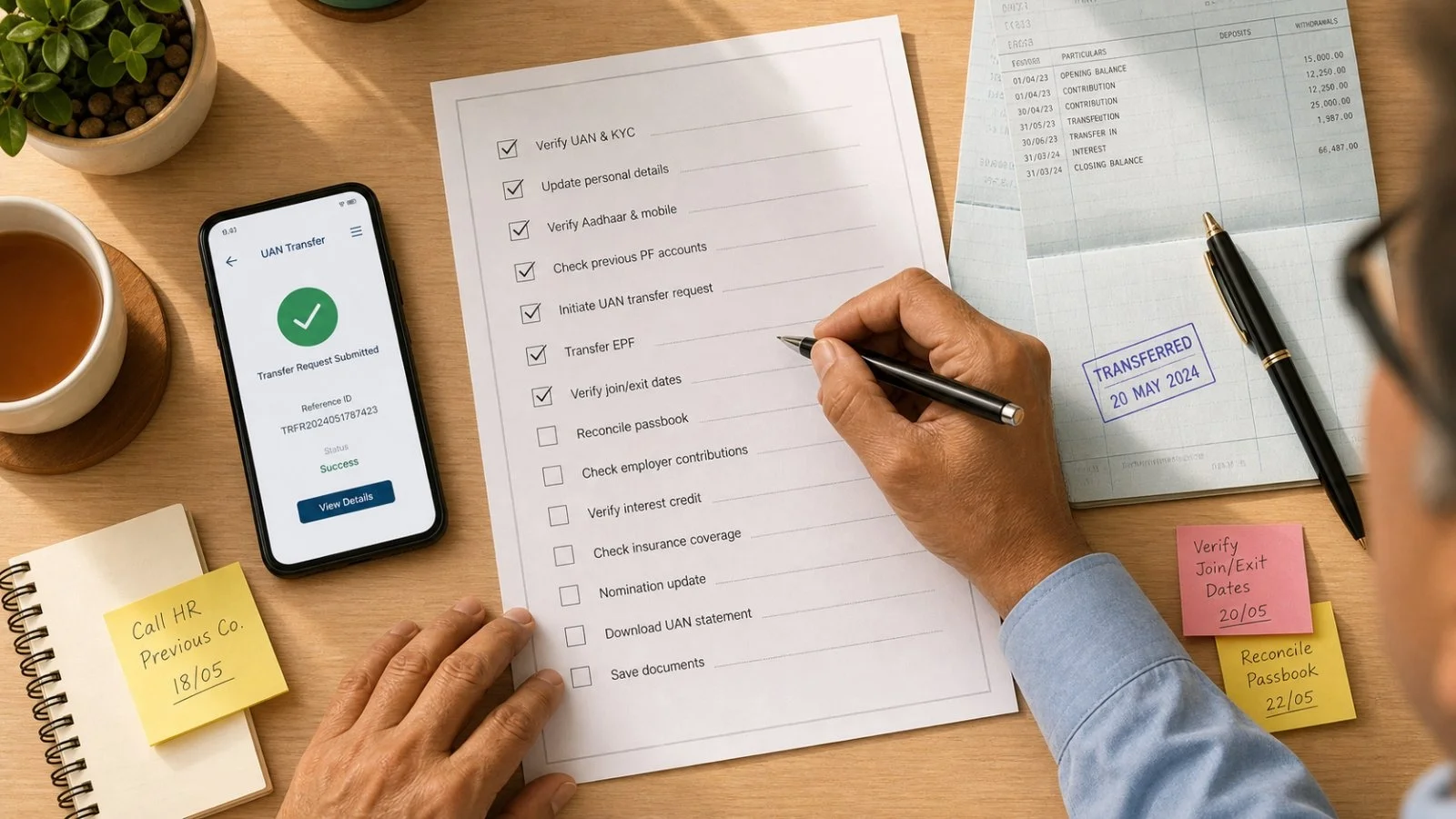

Use this quick action checklist to stay on track:

– Keep your passbook updated and reconcile entries

– Transfer EPF on job change via your UAN

– Avoid premature withdrawals without a goal

– Verify join and exit dates to protect pensionable service

– Review EPFO rules before any major decision

EPF is meant to be a secure, predictable safety net, based on rules. Knowing that interest continues for up to 3 years after you last pay in, inactivity only begins after 36 months, and your EPS pension is available from 58 can stop you from making costly mistakes. For people saving, being clear about this isn’t a luxury; it’s a way to make your money grow even faster.