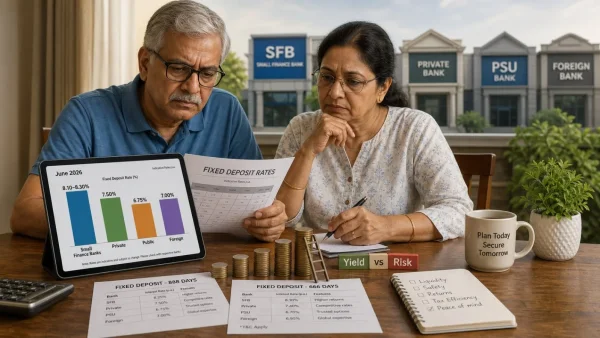

When it comes to where you put your fixed deposits in June, the gap between one bank and another is no small matter. Small finance banks are putting out the best offers. You won’t see that from the likes of SBI, HDFC, PNB, ICICI or Axis. For those of us over 60, there’s a good opening to be had with rates as high as 8.3%.

It’s a simple equation. You get more from the smaller players; you get peace of mind from the larger ones. Since every bank has its own way of pricing in tenure and security, there isn’t one clear winner. You just have to make sure the FD fits your plan.

What the June rate landscape signals

For a 1- to 5-year term, the small finance banks are at the top of the list with 8.10 percent. If you go with a private sector bank, you’ll see 7.50 percent. Public and foreign banks come in at 6.75 and 7.00 percent respectively.

And when you factor in compounding, those numbers add up. Take Suryoday or Utkarsh Small Finance Bank – they will give you 8.10 percent. A more conventional name like DCB Bank will have you at 7.50. Then you have HSBC capping at 5.50.

Looking at the sheets from June 10, 2026, there are some solid mid-7 percent deals to be found. Shivalik Small Finance has you at 7.80, Jana at 7.77, and you can do 7.75 with Equitas or ESAF.

Senior citizens: top-end yields touch 8.3%

The story is even better for retirees. Unity and Shivalik are both offering 8.3% on their highest FDs. As far as we can tell, that’s as good as it gets right now.

A few others are not far behind. Equitas is at 8.25% for 888 days, and so is Utkarsh for 666. You can get the same from ESAF for a 2 to 3 year term, or from Suryoday for 30 months.

There is plenty of room to move around on the maturity side as well. Ujjivan has 8.05% for a little over 3 years. Jana is at 8% for anything from 2 to 5. AU and slice are on offer at 7.9% and 7.75% for shorter stints.

Large-bank benchmarks for retirees

On the private side, DCB is the one to watch for seniors, with an 8% rate for certain tenures like 24 to 60 months. The rest don’t come close: HDFC is at 7%, ICICI at 7.1%.

The public sector is a bit more conservative but still has its moments. Bank of India is at 7.45% for a 3-year lock-in. SBI’s 5 to 10 year option is 7.05%. Canara and PNB are both at 7.1% for their top tier.

Then there are a few other figures to keep in mind. Here is how the rates are shaping up: you’ll see Indian Bank at 7.3% for 555 days, and Punjab & Sind Bank offering 7.25% on a 666-day term. Union Bank of India and the Bank of Maharashtra are both at 7.15%, though the latter is for 400 days. Then there’s the Indian Overseas Bank with 7.1% over 444 days, the Bank of Baroda at 7% for anything from 5 to 10 years, and the Central Bank of India at 6.75% for the 2- to 3-year mark.

Standard FDs: where 1-5 year rates top out

Even if you don’t qualify for senior citizen rates, there is plenty to pick from. DCB Bank is as high as 7.50% p.a., with IDFC FIRST and CSB Banks in at 7.35%. SBM Bank India is also on the table at up to 7.30%.

If you look at the small finance crowd, the numbers are even better. You have Suryoday and Utkarsh at 8.10% p.a. or so. Shivalik is at 7.80, Jana at 7.77, and both Equitas and ESAF will go up to 7.75.

The public sector has a bit less room to move. Indian Bank’s best is 6.80% p.a., followed by Punjab & Sind at 6.75 and the Bank of India at 6.70. The Bank of Maharashtra and Union Bank of India are tied at 6.65, while Canara Bank’s top end is 6.60.

Foreign banks are in a middle ground. Deutsche is at 7.00, Standard Chartered at 6.60 and HSBC at 5.50.

Safety, tenure and the trade-off

But the figures don’t tell the whole tale. What you see in the rate is a mix of the bank’s type, its deposit targets and how it’s funding itself. It pays to be careful not to just run after yield.

Think about your cash flow first. A good rate for 30 months doesn’t do you any good if you’re going to need to break the FD in a year. Laddering your maturities can be a way to hedge against rate changes down the line.

A few things to put on your list before you decide:

– Make sure the maturity fits what you have to pay for

– Do some legwork and check at least three banks

– See what the penalty is for an early exit

– Get clear on how and when you get paid out

– And always recheck the rate right before you book

For older investors, the extra percentage point is no small matter. Over a few years, 8.3% versus 7% is a difference you can see in your post-retirement income. And nailing down a specific term like 888 or 666 days is how you get into the best slabs.

What to keep an eye on

These are the numbers as of June 10, 2026, but they can change in a hurry once banks recalculate their costs. Make sure you have the latest on the books when you are ready to put money in, particularly for any time-limited offers.

How you put your portfolio together is just as important as the headline rate. You can have a core in one of the big names and put some in a smaller, higher-yielding place to get the best of both worlds. If you are risk-averse, stick with what you can hold to term.

There is no such thing as a one-size-fits-all here. The market in June is for those who are precise. Whether you are going for 8.10% at a small finance bank, 7.50% in the private space or 6.75% at a PSU, the only one that matters is the one that makes sense for you.