In an effort to put an end to the chatter, PhonePe has made it clear: we’re not touching bank accounts or UPI. The take for an investor is one of risk containment. By ring-fencing the fee to the wallet, any fallout is kept in the prepaid layer and away from the UPI side of things.

Why this matters for investors

You can see the customer risk being corralled to one product. Even if there is some pushback or churn, it will be with the odd dormant wallet, not with the UPI activity that is the backbone of the brand.

Then there is the matter of making money. PhonePe points out that inactivity fees are par for the course when it comes to offsetting the costs of compliance and operations on a lapsed account. It is cost recovery, not a new tax on your active payments.

What the fee actually applies to

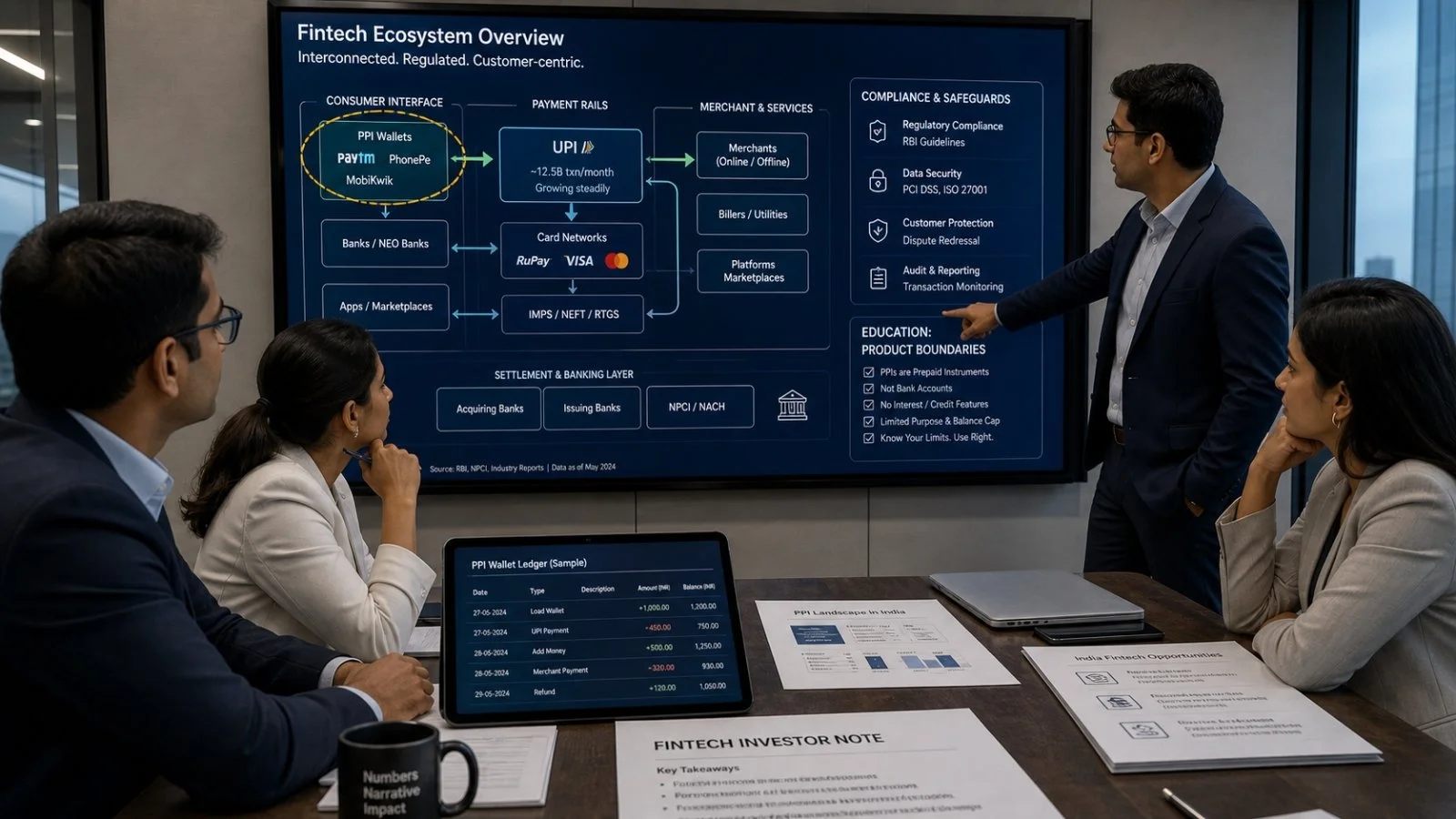

The notifications are for the PhonePe Wallet, which is a PPI. They don’t pertain to UPI, where the funds come straight from your bank.

There is also a hard line: no deductions from a linked bank or via UPI, and your wallet won’t be allowed to show a negative. You have 15 days’ warning before anything is taken from your balance.

Put simply, here is what the company is saying:

– We are only talking about the PhonePe Wallet

– UPI and bank accounts are off the table

– Your wallet balance will not be in the negatives

– A 15-day heads-up is always given

Why active app users still get inactivity alerts

It can be a point of contention for those who use the app to pay for things on a regular basis. But as PhonePe will tell you, they track the wallet and UPI as two different things. You may be using UPI for a QR code or a bill, but the wallet is sitting idle.

And that gets to a common misapprehension. A PhonePe account, a UPI handle and the wallet are not the same. If you treat them as such, you won’t understand where a fee is coming from.

Cashback is not wallet money

For the most part, cashback is put in a gift card balance, not the wallet. So getting some rewards doesn’t make a wallet “active” and it won’t be chipped away at by inactivity rules.

That goes some way to explaining why you might get a notice even after you’ve been in the app for a reward or two.

Reactivation options and customer choices

If you want to put a wallet back in play, it’s not a hassle. You don’t have to go for a Full KYC. An OTP and a transaction will do in most instances.

Those who have been told about a fee have a few ways to go: put some money in, pull some out, or just close it. The 15-day window is there for you to make a call.

Industry context and what to watch next

This is how it is done in the industry for PPIs. The inactivity charge is to cover the overhead of a dormant account. And it has nothing to do with UPI, which is a separate animal that debits the bank directly.

The bottom line for all is to be practical. Know the difference between a PPI and UPI and decide if the wallet is worth it. With the fees and the notice period in place, there is little near-term risk to UPI numbers as the company works to close the gap in user understanding.