It may seem like a short cut to put in your ITR before the Form 16 comes in, but in practice it can tie up your refund, bring on notices and put a crimp in your cash flow when you don’t need it. We are in the filing season for AY2026-27 with 31 July 2026 as the hard stop, and where the risk is, is in being right, not being fast.

These days the tax system is set up to compare what you file with what the government has on file. Mrinal Mehta of BCAS will tell you that while there’s nothing illegal about filing without the form, it is not kind to errors. If your figures don’t jibe with official records, you can expect a demand or a held-up refund.

Why this matters for salaried investors

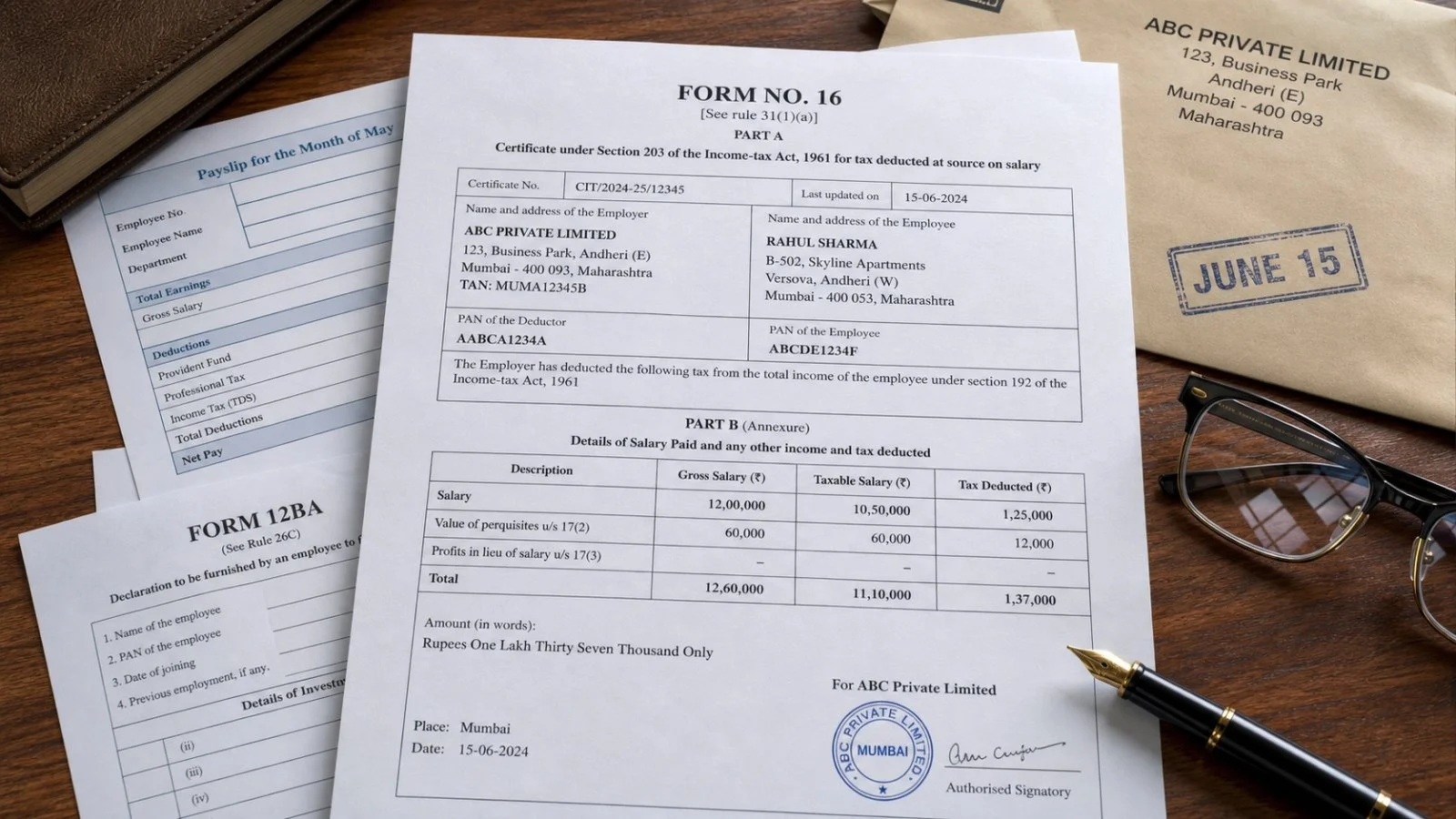

Think of Form 16 as more than a run-down of your pay. It is a TDS certificate under Section 203 of the Income Tax Act, 1961. It puts all your salary, perquisites, allowances and deductions in one place, which is what you want for a return that holds up to scrutiny.

By the books (Rule 31(3) of the Income Tax Rules), employers have to hand over the form by 15 June. They don’t always make it in time. Siddharth Deb, a tax partner at EY India, says you can file without it, but having it in hand makes for a smoother process and less rework. If they are late, they are on the hook for a Rs 500 a day fine.

Key risks if you file without Form 16

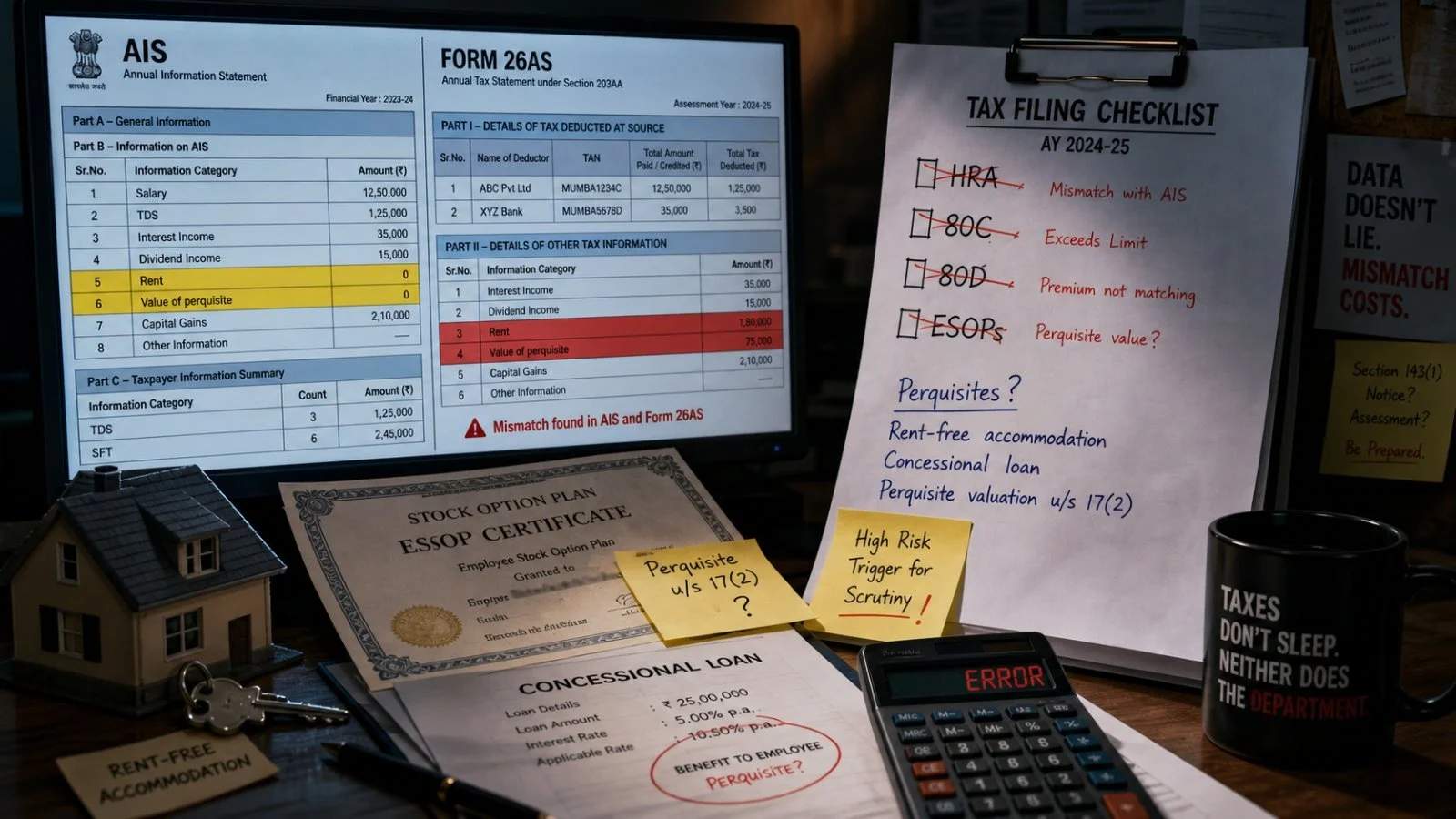

Left to your own devices, you have to piece together your salary from here and there and make it fit with what the Department is seeing in the AIS and 26AS. That is where you are most likely to make a mistake and get a flag on your return.

Here are some of the usual suspects:

– Salary or TDS that doesn’t add up in the AIS or 26AS

– A 80C or 80D claim you forgot or got wrong

– HRA or 24(b) interest not put in right

– ESOPs and perquisites left out of the income side

– Donations (80G) not handled properly

– Overlooking bank interest, dividends or capital gains

The trickier ones are with perquisites and equity-based pay. Things like a rent-free flat, a soft loan, expat perks or ESOPs have to be reported with some exactness. You’ll find them in a Form 12BA or Part B of the 16. Leave them out and you’re asking for trouble.

Then there is the non-salary income. It is all there in the AIS, but not in your payslip. If you miss some FD or bank interest, a dividend or a bit of rental income, you are under-reporting and will be hit with interest and a penalty for it.

What to do if Form 16 is delayed

Don’t just sit on it, but don’t put in a return based on a hunch either. Mehta’s view is to go with the data the government has and then work back from your own papers to build out the salary details as best you can.

Run through this before you hit submit:

– Go over every line in the AIS and 26AS

– Put your salary back together using payslips and the bank

– Have your vouchers for any deductions or donations to hand

– Get the home loan and rent receipts in order

– If the 26AS is missing a TDS entry, nudge HR

– You’ve had more than one job? Make sure to combine the income

When in doubt, or if your package is a bit complicated, talk to a CA. Filing sans Form 16 is fine, but you have to be on top of it. Do it right and you won’t have to deal with a notice down the line.

Inside Form 16: what investors should know

There are two sides to the form. Part A has the PAN, TAN and the TDS. Part B is where you see the full break-up of your pay, the exemptions and how the tax was worked out. Any perquisites will be in a 12BA as well.

It is a handy way to make sure you haven’t missed anything. Deb would be the first to say it is better to wait for it. It makes the ITR a no-brainer and you don’t have to go back and fix things.

Deadlines and the road ahead

15 June is the date for the employer. 31 July 2026 is yours. Even if they are late, you can still file, provided you have the documents to back up your reconciliation with the 26AS and AIS.

For the salaried lot, it is about making a case for yourself this year. A return that is in line with the AIS, has all the income and only the right claims is one that will see your refund come through and keep the penalties at bay. In Mehta’s words, be diligent and you will be better off for it.