The last thing you want this ITR season is a notice of some kind or a refund that never comes. With the 2026-27 filing open, it’s a no-brainer for salaried workers and investors: do the legwork now or deal with the compliance and cash flow headaches down the line. Here is where to put your focus.

There is more to it than just going through the motions. Preparing early is what separates a clean report from one that might be second-guessed. It lets you check that the tax on your PAN is in order, confirm where your income is coming from, and put in for every deduction you can.

Why this is a big deal for investors

Between the capital markets, property and high-yield deposits, you are leaving a trail of data. Your return has to match up with Form 26AS and the Annual Information Statement, or you could be looking at held-up refunds or having to answer some questions.

In 2026-27, it is as plain as day. A well-put-together file means you can put in for your home loan, insurance and other benefits. Leave out a piece of evidence and you leave the deduction on the table.

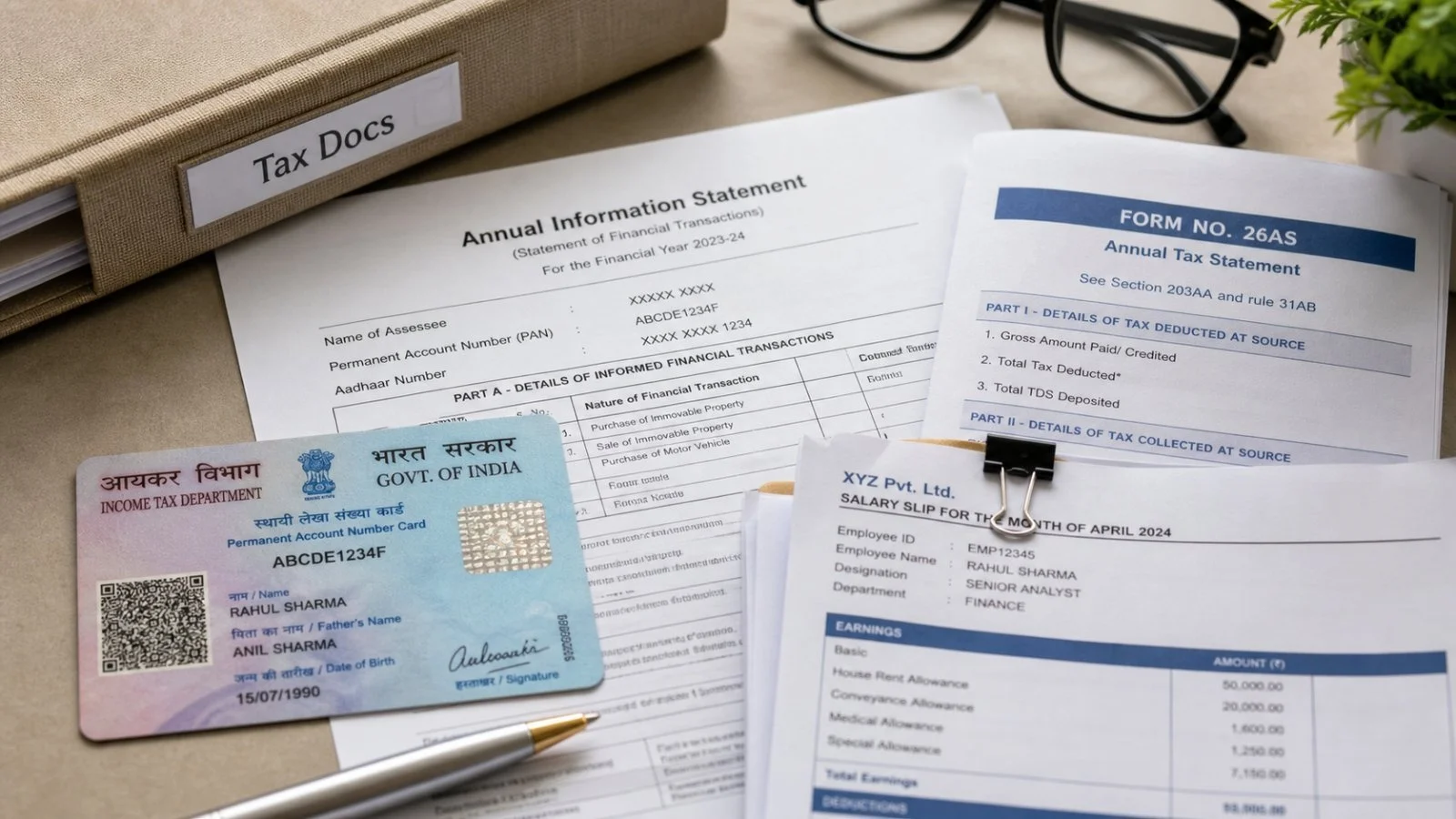

The basics: who you are and what you owe

Start by nailing down the evidence that underpins your return. You’ll need these to put your identity on record and see what has been paid against your PAN. Have them to hand:

– Your PAN to map out tax credits

– Form 16 to back up salary and TDS

– Form 26AS for TDS, TCS and any advance tax

– The Annual Information Statement for a view of your transactions

– Pay slips for the fine print on earnings and allowances

– Bank statements to square away interest and the rest

– Books of Accounts if you have a business or professional side to things

– NRE/NRO info for any income from overseas

With several income streams, these are what will keep you from under-reporting and help you make sense of your numbers.

For those on a salary

Your first port of call should be Form 16 and your monthly slips. They are what you use to verify what was put in your pocket and what the employer has already taken off for tax.

Are you taking House Rent Allowance? Then have your rent agreement and receipts at the ready. In some cases, you may have to produce your landlord’s PAN as well. Don’t let the paperwork for any other exemptions from your employer slip by.

If you run a business or are self-employed

Freelancers and the like have to live by their records. Thorough notes are your defence for computing income right and for when you are put to the test on compliance.

Hold on to your invoices, the books, and any financials. GST returns, proof of advance tax and anything that shows your professional income should be in the file.

It is how you prove your expenses and figure out your taxable profit from the Books of Accounts.

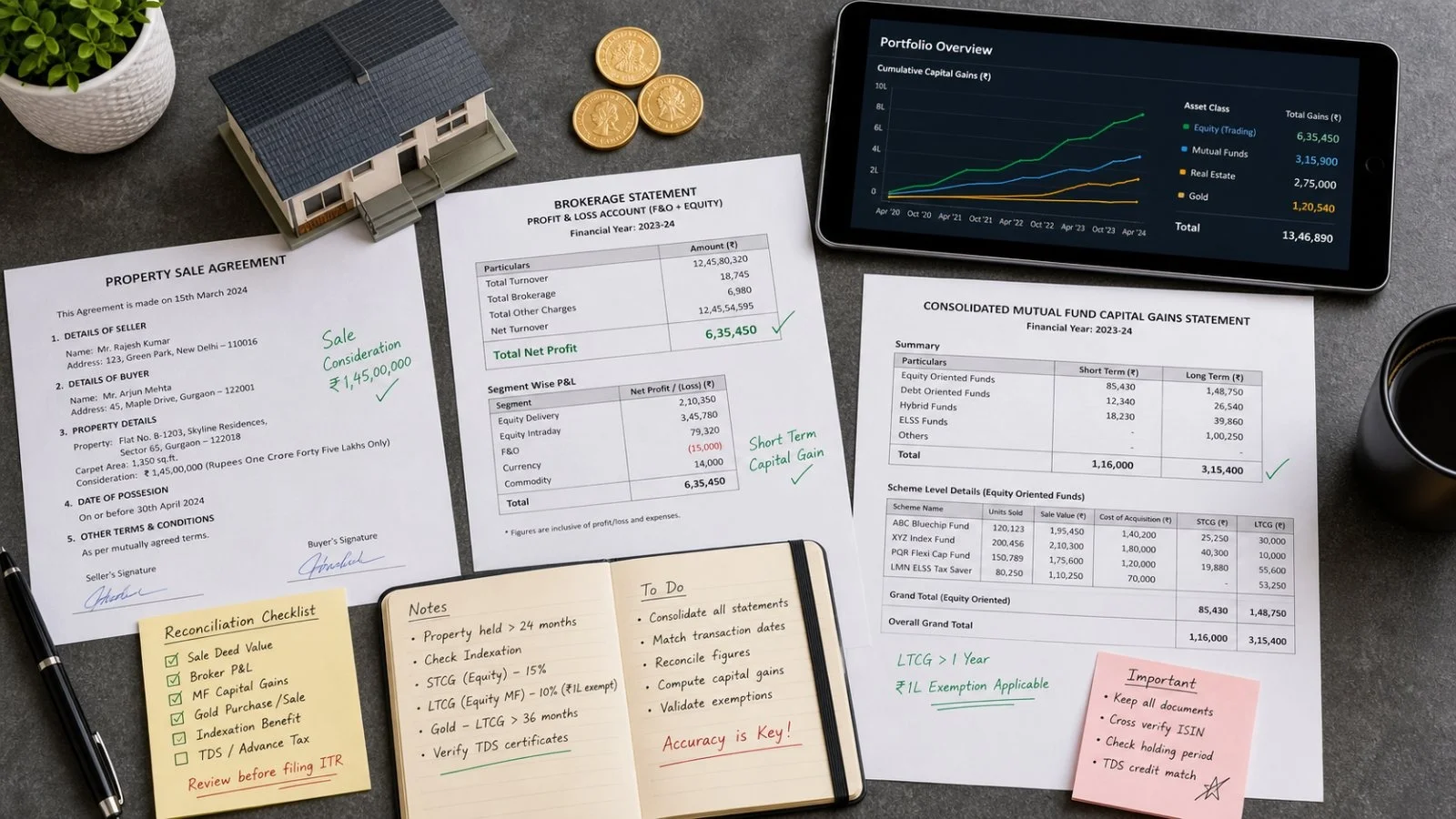

On the subject of capital and investments

You have to declare any move of a capital asset, win or lose. Be it a house, some shares, a bond or gold, it all has to be put in.

When it comes to property, make sure you have the sale and purchase papers, the address, and a record of the costs you put in during the transfer. Don’t forget to have the buyer’s PAN and Aadhaar on hand.

When it comes to shares and mutual funds, you can’t do without the consolidated capital gains from your fund house or the P&L and capital gains statements your broker will put out for you.

Here is what you should have at your fingertips to make things run smoothly:

– Agreements for any property you’ve put up for sale or bought

– Any expenses tied to a transfer

– The nitty-gritty on the property’s address and ownership

– The buyer’s PAN and Aadhaar

– Consolidated capital gains for your mutual funds

– Reports from your broker on profit and loss

You need these to figure out your capital gains with any degree of accuracy. Without them, you’re prone to under-reporting or inflating your liabilities.

Interest, dividends and bank-linked income

Put aside your main source of income for a moment; you still have to account for interest and dividends. Your bank and the platforms you use will show this, so it’s important to reconcile.

Your bank statements are a good way to spot taxable credits over the year. Hold on to the interest certificates for your fixed and recurring deposits. If TDS was taken out, keep those papers. And be sure to get dividend statements from the companies and funds you hold.

Running these by the Annual Information Statement is the best way to avoid any hiccups in your reporting.

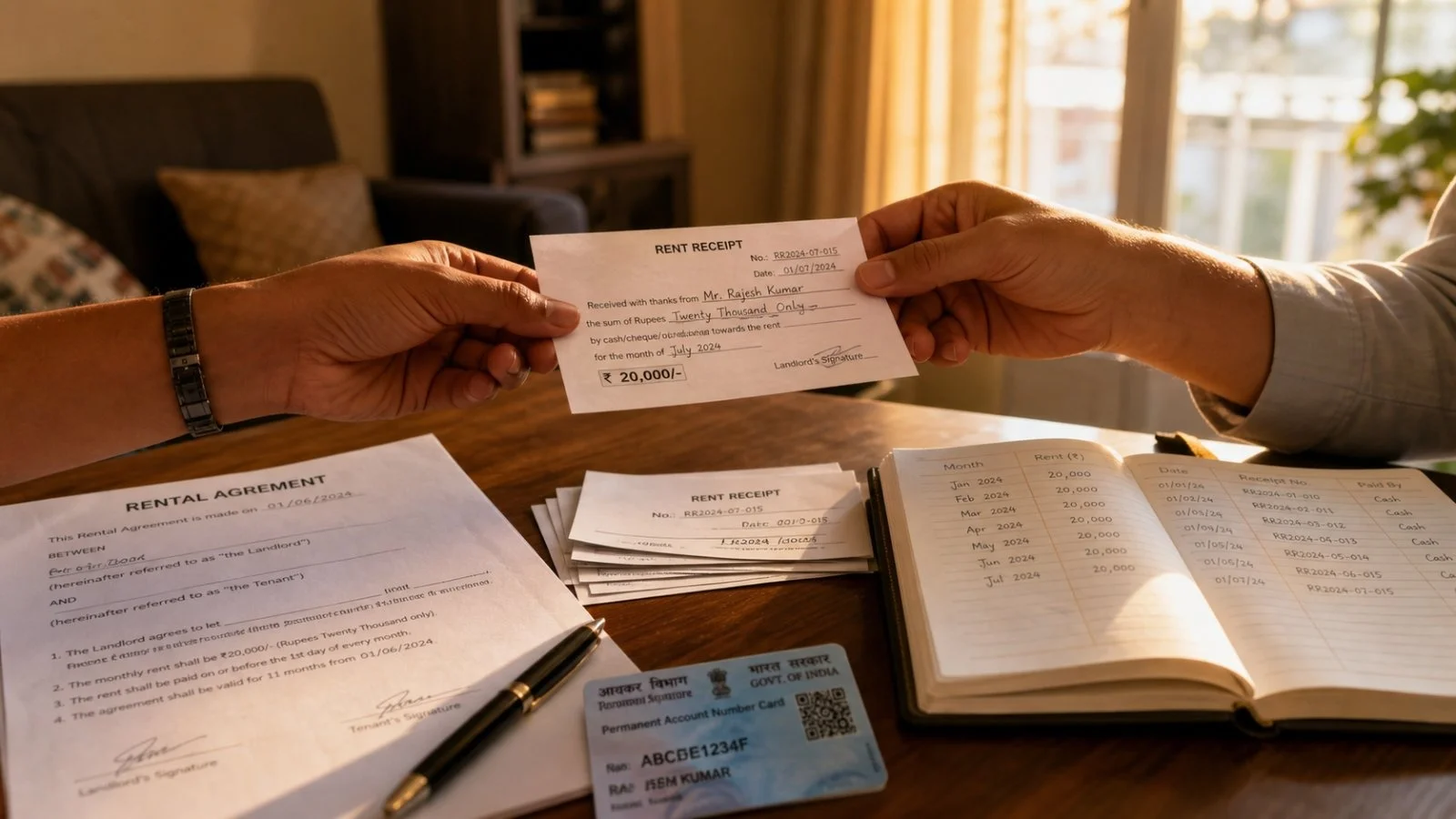

Property income and home loan benefits

Rental income is on the table for tax, so you need to back it up. Have your rent agreement, a record of what you’ve been paid, and the tenant’s PAN and Aadhaar if you can.

For home loan perks, you’ll want the interest certificate from your lender. You may also be asked for municipal tax receipts to vouch for your claims. All of this adds up to a proper calculation of your property income and lets you take the deductions you’re owed on the principal and interest.

Proof for deductions that make a difference

The right kind of documentation can put a dent in your tax bill. File without it and you might find your claim turned down.

So keep the evidence for your PPF, ELSS, life insurance and even tuition. For Section 80D, you’ll need your health insurance premium receipt. Education loan interest for 80E? Have the certificate. NPS contributions? Put the statement in a file. It’s the only way to be sure you’re not leaving money on the table.

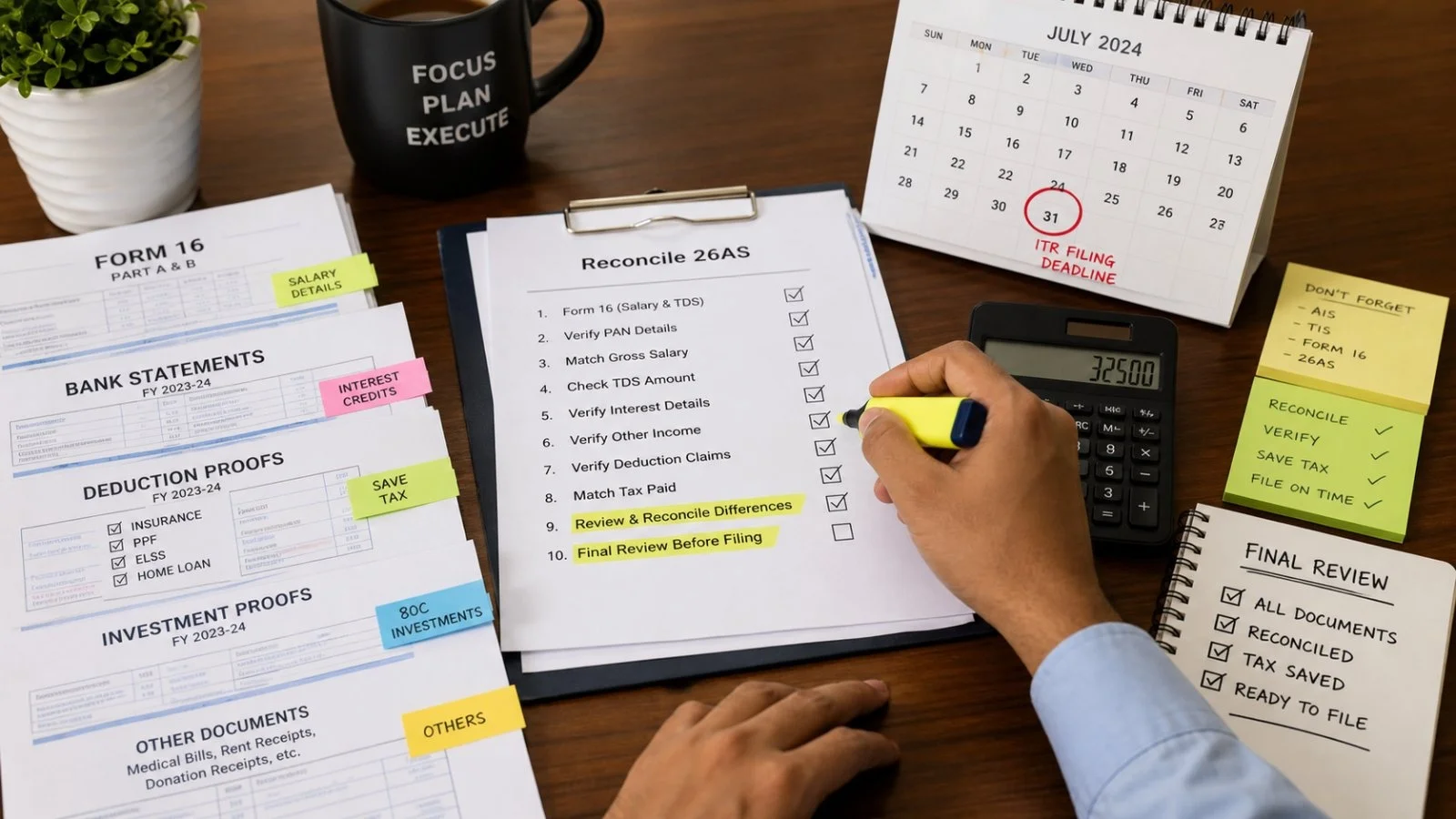

How to go about it

Start with some legwork. Reconcile the numbers in Form 26AS and the AIS with what’s in your bank, your Form 16 and your investment records. After that, add in your deduction and property details. A final pass over your rent and business files for anything you may have left out.

Do it this way and you’ll have less rework. With a solid paper trail, you lower the odds of an error or a close look from the authorities, and you’ll be in a better spot to see a refund come through.

If you’re in a rush, focus on the basics first. Most of the time, discrepancies come from unreported interest or capital gains, or when your proof doesn’t line up with what you’ve put down.

What it all means for AY 2026-27

Filing for 2026-27 is where you are made or unmade. The upside is in making sure you’ve got every exemption and deduction you can. The downside is in the fine print of your transactions – something active investors and those with property should be wary of.

*We put this together for your information. For the most current rules, we suggest you speak to a tax professional.*