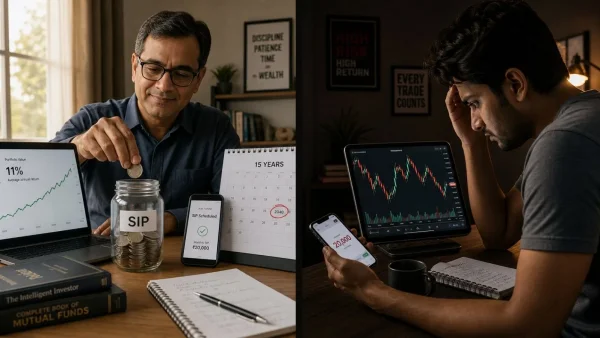

So you’re mulling over a Rs 20k SIP in a volatile fund versus a heftier one in a no-nonsense option. It’s a crossroads with some weight to it. The thing that moves the needle isn’t the return on the page, but the amount you put in every month. If you do the numbers, you’ll see that a larger SIP can de-risk your plan without you having to lower your sights.

The core risk: underinvesting, not underperforming

Most of us are in no danger of missing out on the one hot fund of the year. The problem is we put in too little and count on some big return to make up for it. But the market doesn’t oblige. Too much confidence can hide the fact that you haven’t put in enough.

Save at a higher rate and, boring as it may be, you build some real leverage. You can’t simply outperform an underfunded plan, but you can save your way to a better one. For any household with a goal in mind, that’s the bottom line.

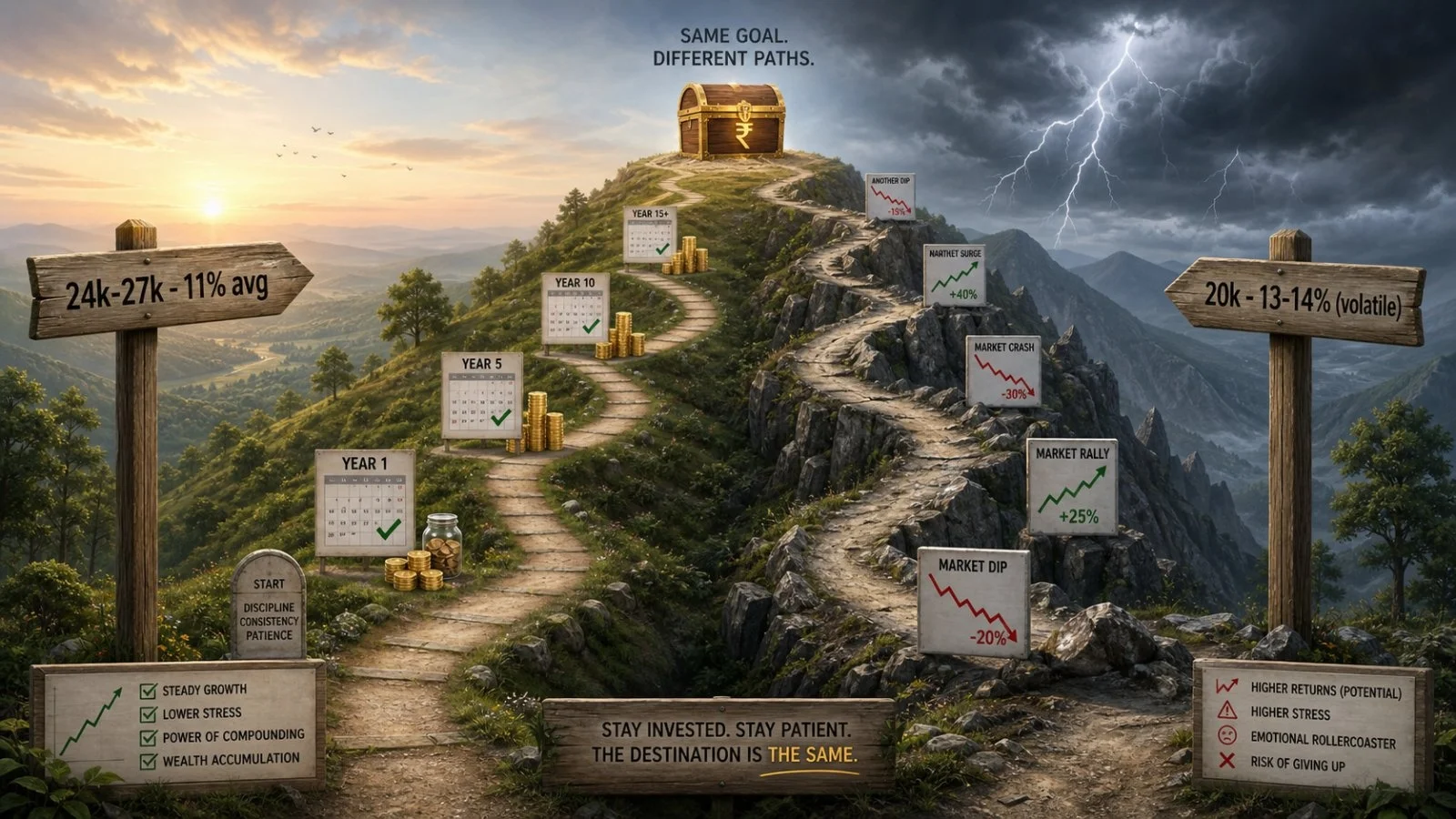

The trade-off in numbers: same corpus, different paths

Work from the end result back to where you are. Let’s say you want to be sitting on Rs.1.1-1.2 crore in 15 years. One way to get there is with a 11% average from a safer instrument. That means a monthly SIP in the neighbourhood of Rs.24,000-27,000.

Then there is the other side of the coin. You put in Rs.20,000 a month for 15 years into something with more bite, one that might give you 13-14% on average. On paper, you come to the same Rs.1.1-1.2 crore, provided those returns hold up.

It is more than just the math; it is your risk tolerance. In the first case, you are putting in more for a steady 11%. In the second, you are betting on 13-14% while investing a smaller sum of Rs.20,000. Whether that happens is another story.

What the SIP math implies

– You can trade off return risk for the discipline of saving

– Bump up the SIP and you don’t have to rely on alpha you can’t be sure of

– A return target is what you hope for, not what you are owed

Concentrate on what is in your hands and you are less exposed. You can always tinker with your earnings or outgoings to change your SIP. Market returns are not so easy to manage. In the end, this is what makes for a predictable outcome, not the product you pick.

Why relying on high returns is an expensive habit

There is nothing wrong with setting your sights high. But if you make it a crutch, your plan will fall apart. You can have a couple of good years. To do it over and over with some kind of system is hard work and takes a lot of mental energy.

Funds that tout better returns are built with more risk. Every now and then that risk shows its face. When it does, investors tend to get jumpy and make the wrong call. You don’t factor in that kind of cost when you start out.

Look at it from this angle and a larger SIP is not a concession. It is being smart. You are making the odds work for you by turning up the volume on what you know, instead of counting on the market to hand you 13-14% right on time for the next 15 years.

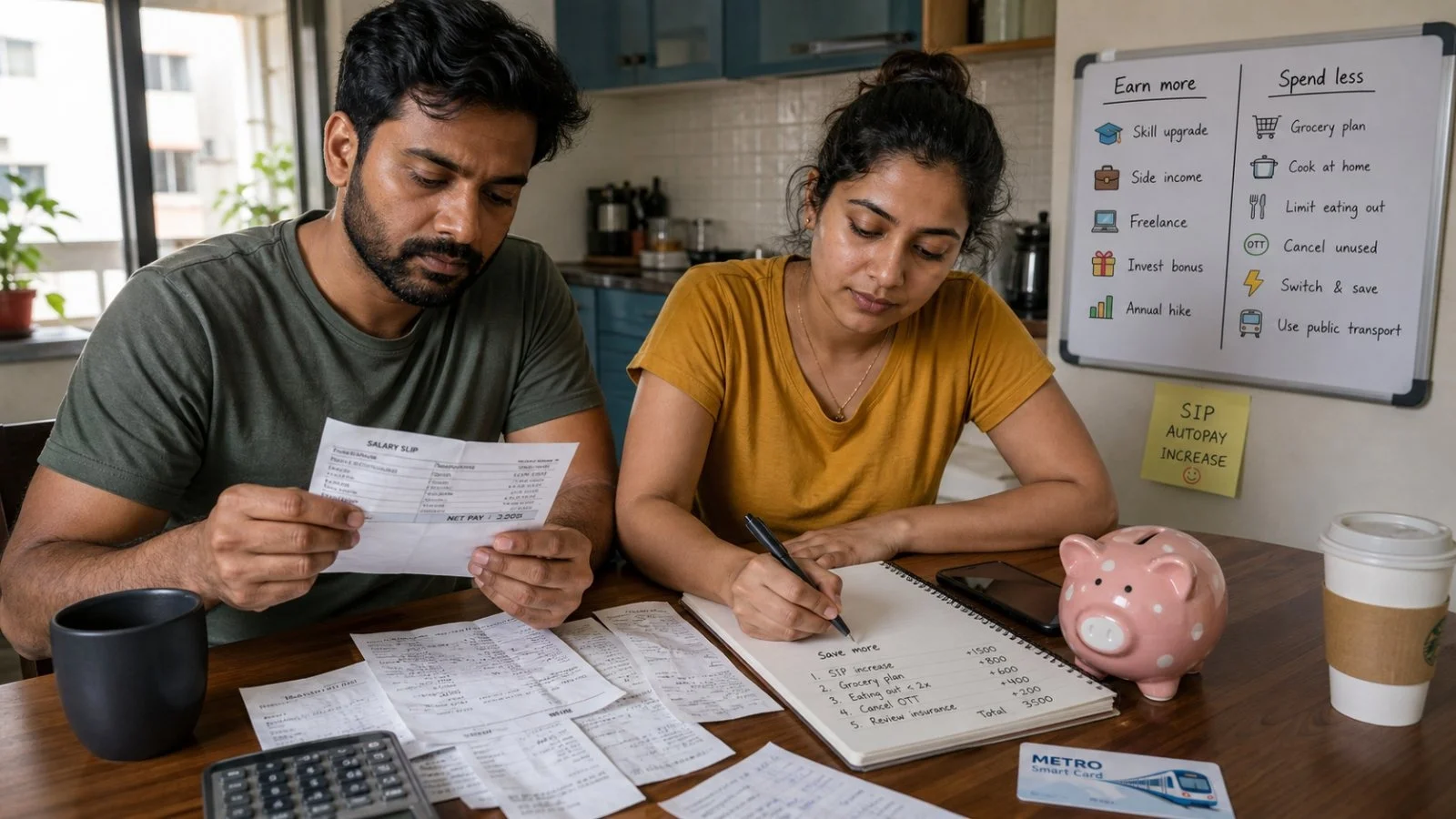

How to fund a higher SIP without derailing life

It is simple to tell someone to put in more. The hard part is making the cash flow happen.

For the average home, there are only two dials you can turn: make a little more or put out a little less. What’s left over is your savings.

When hard constraints don’t leave you with much to work with, you can size up some extra risk, as long as you have a long view and the right temperament for it. But be deliberate about it. Don’t take on risk for the thrill of it; do it because your plan calls for it.

To see if your plan can hold water, run some numbers. The SEBI has a handy calculator (https://investor.sebi.gov.in/calculators/sip_calculator.html) where you can put different return rates to a SIP and get a sense of what’s actually possible in a given month.

Investor impact: the case for a higher SIP

Asking whether to go with a Rs 27k SIP isn’t a matter of shelling out more for the same. It is a way to buy into predictability. Put in Rs.24,000-27,000 a month for 15 years at an 11% average, and you are on track for a Rs.1.1-1.2 crore pot without having to put everything on the line for 13-14%.

You could make a Rs 20k SIP in a riskier vehicle work, but then you are at the mercy of the market. If those 13-14% returns don’t come in, the shortcoming is yours to deal with. You might end up with a goal that is out of reach or have to make some hard lifestyle choices.

If you look at the kind of people who have put together wealth over the years, they didn’t do it by nailing every exit or zeroing in on the one ideal fund. They are the ones who put aside more than their friends, hiked their SIPs when they got a raise, and didn’t flinch when the market pulled back.

How to think about your SIP today

So, when you are weighing a Rs 20k SIP for better returns against a bigger one for steady ones, ask yourself how much let-down you can stand. Is it easier to miss out on a big number or to have to put off something important because you were under-invested?

Then be honest about what you can handle this month. Can you put in the Rs.24,000-27,000 and be disciplined for 15 years at 11%? Or is your cash flow going to force you to a 13-14% chase to hit the same target?

Put it simply:

– A larger SIP means you don’t need to be as lucky

– A smaller one requires the market to outperform

– Being predictable is good for the soul

Make of it a rule, not a one-time thing. Be hard on your expenses, funnel any pay increase into a higher SIP, and don’t panic when things get volatile. That is how you get to your Rs.1.1-1.2 crore.

Where to from here

Do the math on the calculator and pick a monthly amount you can stand behind. If you can land in the Rs.24,000-27,000 range at 11%, you have some control and haven’t compromised on the end game.

If you are stuck at Rs.20,000, be clear on the risk of aiming for 13-14% on average. Set up some buffers, set it on auto, and don’t fiddle with it. The market isn’t going to give you above-and-beyond returns just because you’re saving a bit. In the end, the size of your investment is what counts.