You can move the needle on your outcomes by lakhs with just a tweak in how you put your money to work. Run the numbers on a Rs 5 lakh one-off against a Rs 5,000 a month over 8.3 years at 12% and you’ll spot a performance difference as well as a risk one. It’s not so much about the arithmetic as it is about temperament and when you make your move.

Why the way you go about it is important

Money that gets to work early is the kind that compounding will reward. With a lump sum, you’re in from day one, giving you more time in the market. Should the cycle turn in your favour, the gains build up fast.

SIPs are the other side of the coin. You put in a little at a time, which softens the blow of a bad entry and smooths out the market’s moods. It’s a trade-off that can be the difference between staying put and bailing out when things get volatile.

A case for looking at both sides

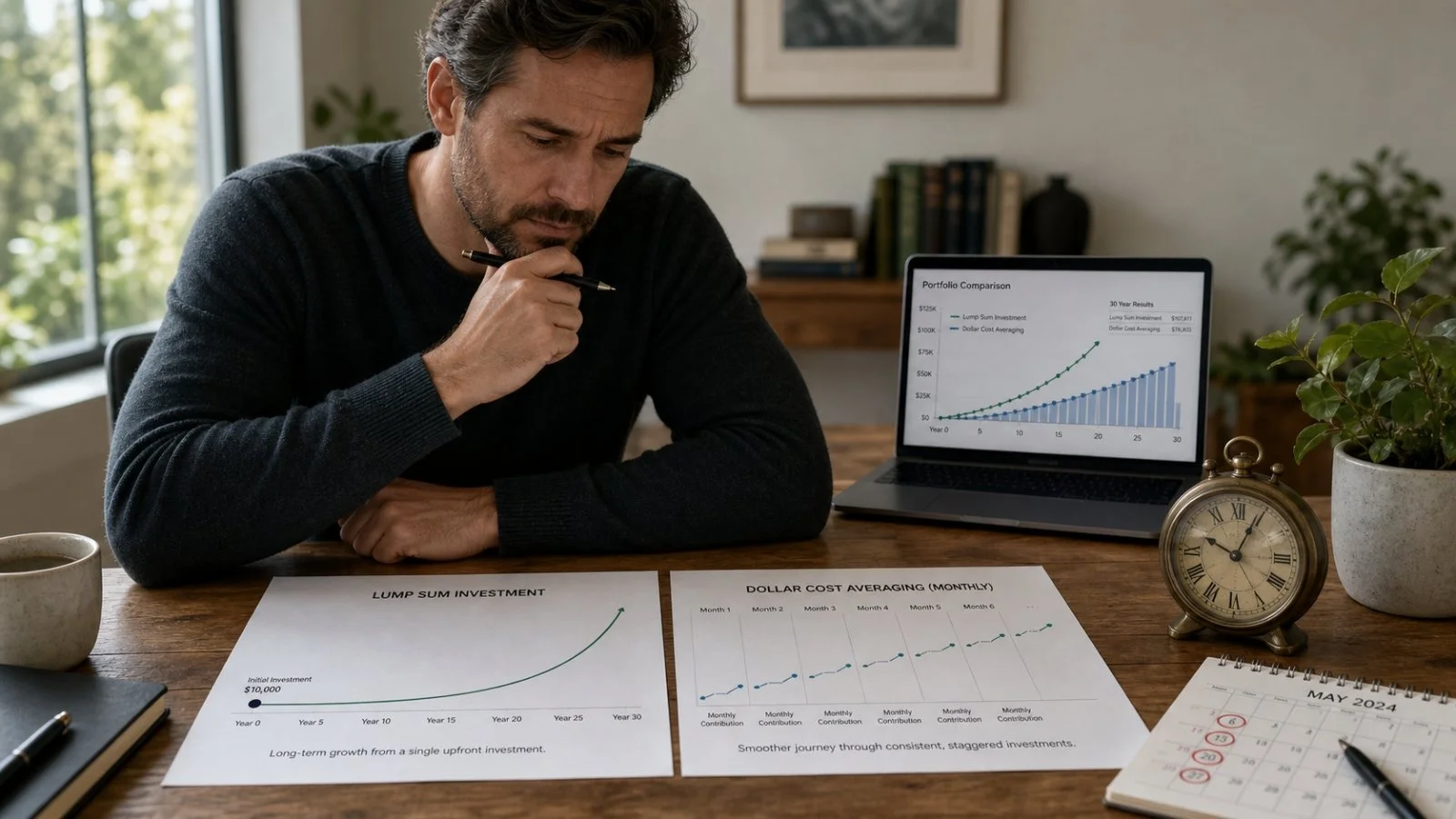

Take our first example with the same period and return in mind. A monthly SIP of Rs 5,000 for 8.3 year at 12% means you’ve put in Rs 4,98,000. You can expect returns of some Rs 3,57,505, for a total of Rs 8,55,505.

Then there’s the one-and-done approach. Put in a lump sum of Rs 5,00,000 for the same 8.3 year run at 12% and while the principal is the same, the returns are estimated at Rs 7,80,794. You’re left with a total of Rs 12,80,794.

What puts the distance between these two is the time you have in the market, since the return and duration are the same. Having more capital at play from the get-go is what makes for a fatter corpus.

What 100 months of this looks like

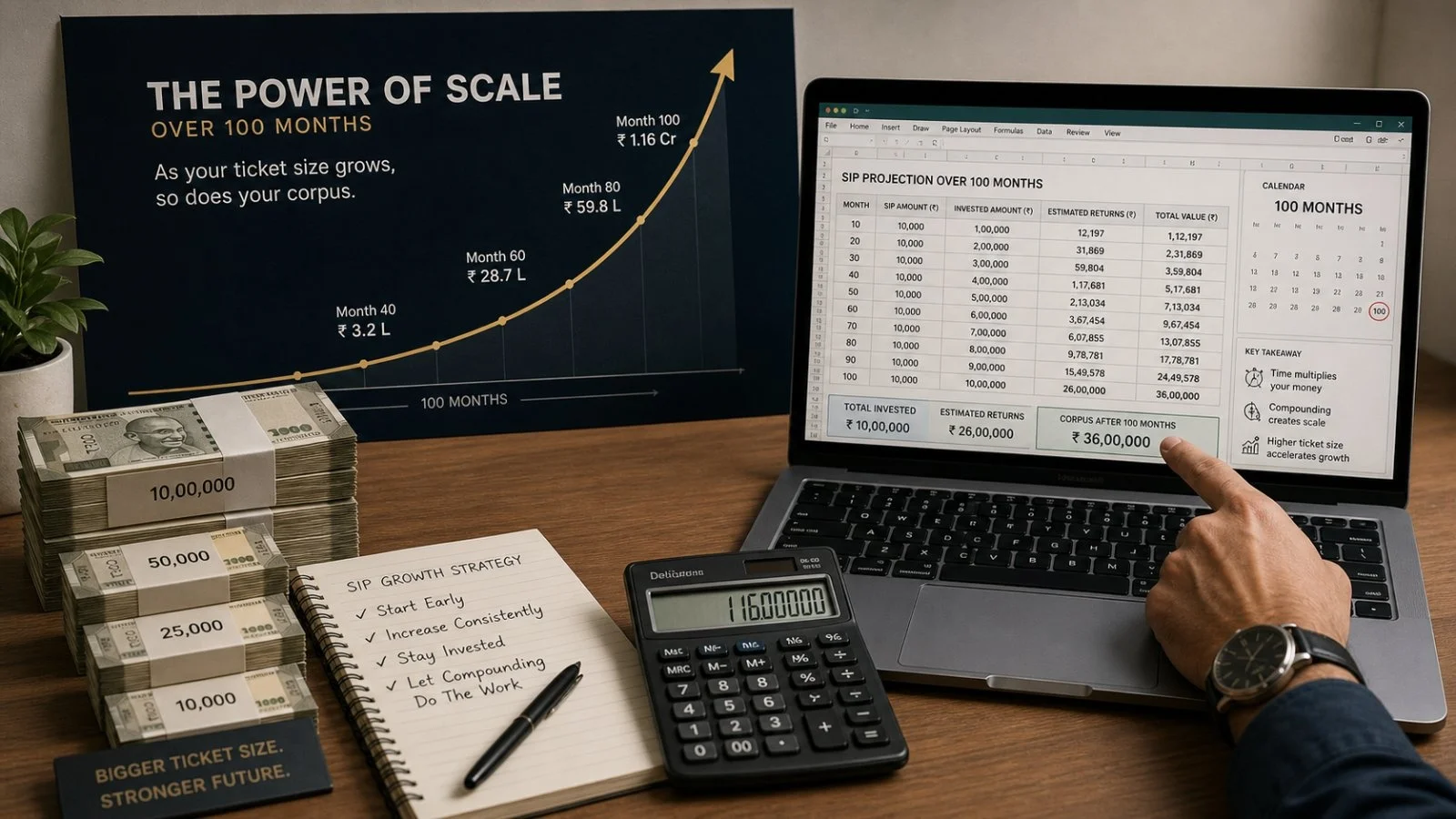

We’ll do another run with the 100-month (8.3 year) mark and 12% return, but with a bigger number. If you invest 10,00,000, the illustration has your returns at 15,71,285. It’s a good reminder of how the compounding machine picks up speed as the size of your ticket does.

But for an investor in the thick of a drawdown, the experience of a lump sum and a SIP can be worlds apart. Staying the course is what counts.

Risk and opportunity: where you stand

Going in with a lump sum is a concentrated risk. Markets can give way right after you put your money in and you’ll see the loss across the board. Some with a long view and the fortitude to look past short-term wobbles are fine with that.

With an SIP, you have your entry points spread out. It takes the pressure off to be right on timing and can make the market seem a bit less of a threat. For those who prefer a lower or moderate level of risk, it’s a more comfortable way to go.

Making it fit your finances

For most on a salary, an SIP is the natural fit; it follows the paycheck. But a bonus, an FD coming due, or an inheritance will have you thinking in terms of a lump sum. The right call is a matter of your goals, your buffers and how you handle volatility.

Do a few reality checks before you decide:

– Line up the horizon with when you need the money

– Be honest about whether a dip would make you panic

– Make sure you have an emergency fund on the side

– Let your cash flow dictate the method

– Don’t try to time the market if you can’t back it up

The examples here are for show, under the same conditions. They make the point that, on paper, you build a larger pot if you let compounding work from the start. But they don’t do the job of managing your emotions or the market for you.

In a downturn, the one who panics and sells a lump sum may be in a worse position than the one who kept up with his SIPs. On the flip side, a patient type can make more of a well-timed lump sum if he can hold on through the cycles.

Where to from here

Get your goal and time frame in order. If you have a sizeable amount and a long way to go, a lump sum is an efficient way to put it to use. If you want to keep things steady and have some room to manoeuvre, an SIP is made for that.

Whatever you do, stick to the plan and the logic behind it. Only re-evaluate when your objectives shift, not because of some noise in the market.

This is for your information. Talk to a registered financial advisor before you make any moves.