In a way, this young Mumbaikar has put a finer point on something a lot of new earners are wondering: is 20,000 in savings a month enough to build a future on? The back-and-forth is as much about being disciplined and controlling risk as it is about the numbers on a page.

You can see why the post, which is his first foray into career planning, has made some waves. It gets at the hard choices you have to make in an expensive city. There’s also a sense of change in how people are thinking; these days, you’re more likely to see a fresh face on the job market with retirement on his mind from the get-go instead of putting it off for later.

What sparked the debate

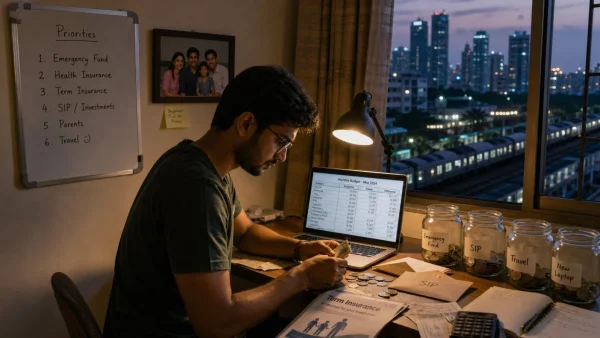

The user says he’s about to start work in Mumbai with a 1 lakh a month and wants to get on top of his retirement plans right away. He sees it as a long game, not something to be made up for in the middle of his career.

He put out a breakdown of his finances and wanted to know if 20,000 in monthly put-aways could be put to good use for both near and far-off aims. Under the heading 'Retirement planning for a 22 year old!‘, he was after some advice on where to put his money, what kind of insurance to get and what to watch out for as a novice.

Why this matters for young investors

With the cost of living on the up, we’re living longer and there is more of a focus on being financially free, so a lot of folks are looking at their options sooner. This is a good example of that: you have a starting wage, you may have to help the family, and what’s left isn’t a lot.

Those who chime in will tell you it’s good to start young, but the order of things is key. Make sure you can weather a storm and have some earning power before you go after returns, they’ll say.

What commenters suggested

You’ll find a lot of agreement in the replies: put a safety net in place and don’t overcomplicate your portfolio. A few are making the case for insurance now, and then moving on to investing once you have some cushion.

There are a couple of things the consensus is on:

– Have an emergency fund for at least half a year of expenses

– Get health and term insurance sorted

– Be simple and steady with your first forays into investing

– Don’t try to fine-tune your products in year one

– You can tinker with your allocations when you’re making more

One person put forward the idea of stashing 5 lakh for emergencies before you get bold with your money. Another had a different take: put 18,000 a month in the till for the rainy day and 2,000 in a SIP to get in the habit of it while you’re at it.

Then there’s the matter of insurance. More than one response was to get a term plan while you’re still young and premiums are low, and maybe add a 10 lakh Personal Accident policy for good measure.

Income growth over micromanaging investments

If there is one thing that comes through, it’s that you should be on to growing your income in the beginning.

There’s a view that you’ll see more of a compounding effect from upskilling, or even making a role change if it makes sense, and haggling for a better salary than you will from moving money around in a small portfolio.

It’s not to say put investing on the back burner. The point is to be a steady investor but put your where your time is: on putting more money in. In the long run, those higher contributions will make any minor gains from fine-tuning your holdings look small.

The numbers behind the worry

This poster is looking at some outflows he can’t get out of. He has 30,000 to send home, another 30,000 in rent for his own setup, and close to 20,000 for food, transport, bills and the like.

You’re left with about 20,000 a month to put away. It’s a good enough start, he concedes, but when you factor in inflation and the price of living in Mumbai, it doesn’t quite add up. On the plus side, he has no debt and nothing big to buy in the near future.

He’s been about as consistent as he can be, ratcheting up what he puts in when his pay does. Most of the feedback was in line with that, so long as you have your insurance and an emergency fund in order before you go after returns.

What it means going forward

When you’re 22, you have time on your side, but also the risk of a misstep. A solid emergency fund and the right kind of coverage can keep you from being derailed. Then you let your contributions grow with your income.

If you’re in a pricey metro, the way you budget is a tool in itself. You’ve got to support family, cover a high rent and meet your needs; it chews into your surplus. So you have to be strategic and build some career headway.

A few things to take from the conversation:

– Put protection first

– Have some cash on hand for the unexpected

– Be regular with your investing, then increase it

– Work on the skills that put more in your pocket

No one here is going to give you a formula that works for everyone. The general line is to have a plan: cover your downside, set up your investing on autopilot and make the most of your earning power while it’s flexible.

You could tell this user has had a change of heart. Retirement isn’t something to think about in your 30s or 40s; it’s something to deal with from day one. Some would say that attitude is as important as the funds you pick.

Then there are those who pointed out that with a modest nest egg, you can easily overthink the perfect asset allocation. Better to just put down a buffer, get the necessary insurance and stick with a SIP, no matter how small.

Some made a point of being clear on your goals. Your retirement and your next few years don’t have the same timeline. If you ring-fence what you need for now, you won’t be as likely to dip into your long-term money when times are hard.

Feeling unsure if 20,000 is enough? You’re not alone. But it’s more about where you’re headed and being able to adapt. Save what you can and put in more as your check gets bigger.

Of course, this is all from a social media thread, so it’s just people’s opinions and we haven’t verified anything. Do your own due diligence and talk to a pro if you can.