If you’re new to mutual funds and have around 10,000 rupees to invest, a financial professional says it’s better to use a Systematic Investment Plan (SIP) instead of putting all the money in at once. SIPs help you get into the habit of investing regularly, lower your average cost, and avoid trying to guess when the market will be at its lowest (which is very difficult!). The idea is to start with a little, invest consistently, and have a long-term view.

Why the entry route matters now

For someone just starting out, getting the highest possible return isn’t as important as reducing the risk of when you first start buying. SIPs spread your purchases over time, lessening the effect of market ups and downs. The money is taken from your account regularly, and your investments grow slowly over time with compounding.

Putting all your money in at once (a lump sum) means all the risk of when you invest falls on a single day. This only really works if the market has already gone down or is correcting. If the market then falls even further after you’ve invested, you’ll see losses right away and that could make you panic.

Expert playbook for Rs 10,000 starters

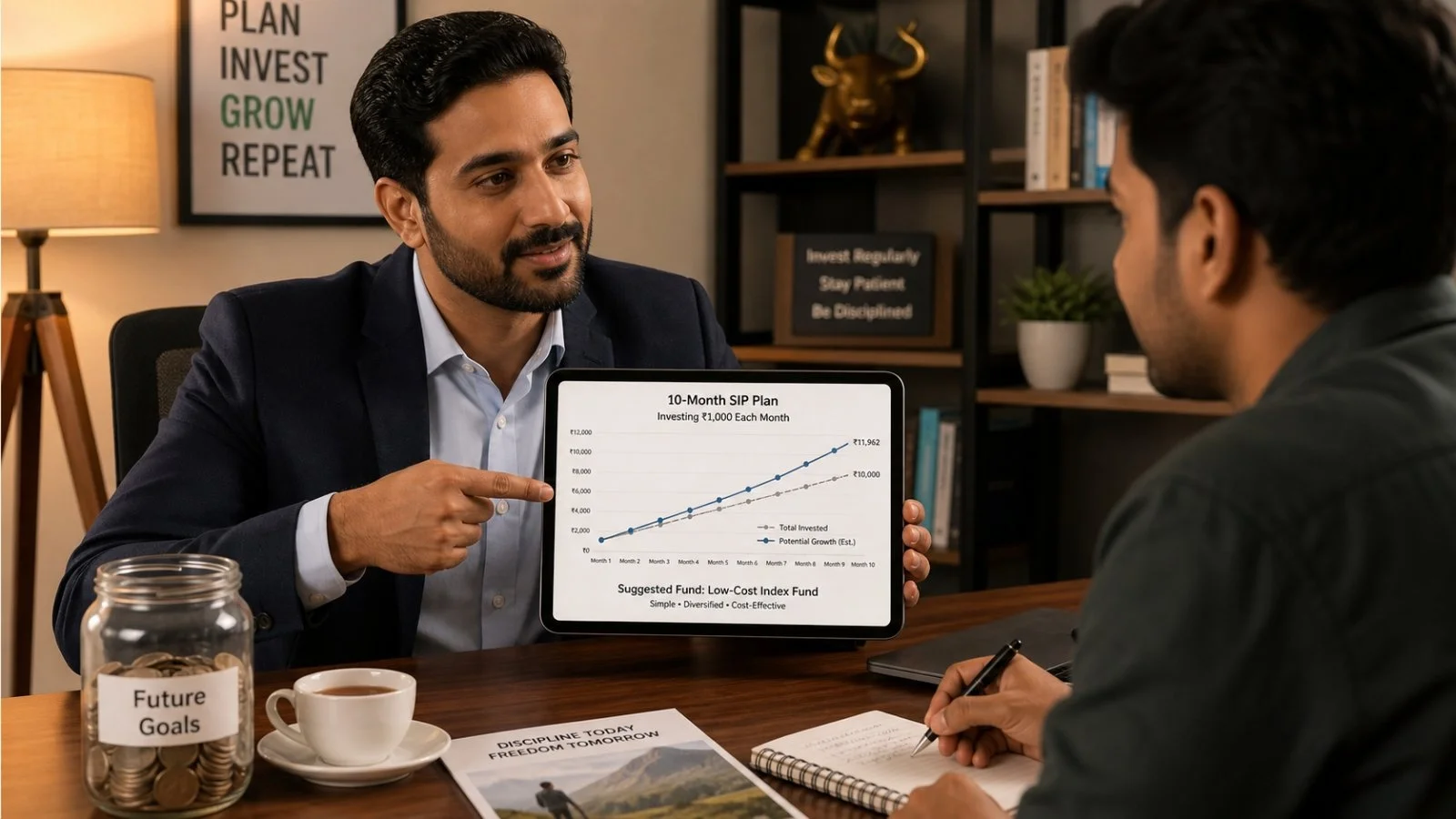

A financial advisor, suggests first-time investors avoid a lump sum at the beginning. He’d rather you turn 10,000 rupees into a 10-month SIP of 1,000 rupees each month. This way, you’re putting money into the market at different prices, and this averages out how much you pay for your investment.

When choosing the fund itself, he says to begin with a cheap index fund that follows a big market measure like the Sensex or something similar. Index funds give you a variety of investments without the difficulty of choosing a fund manager, which is good for beginners.

Expert also says how long you’ll invest is important. Investments linked to the stock market can go up and down a lot in the short term, so you should plan to stay invested for at least 8 to 10 years. This is how long compounding and the market growing will really have an effect.

What a lump sum is good for

A lump sum can do well if you invest it after the market has gone down or is correcting. That’s because prices are often lower at these times, giving room for them to increase. But a lump sum needs you to have money available and to be able to hold it for a long time.

You need to be able to handle risk and have patience. If you put all your money in right before the market drops again, it can be very discouraging and many beginners find it hard to keep their investments. And if you might need the money soon, a sudden market fall could force you to sell at a loss, making things even worse.

Blending strategies without timing the market

You don’t have to pick one method and stick with it. Many people have a regular SIP and then add more money when the market goes down – this is called ‘buying the dip’. This lowers the average price of your portfolio and can improve returns as prices recover.

A Systematic Transfer Plan (STP) is another way to get from a lump sum to a SIP. First, your money goes into a very safe, liquid fund (easy to get your money out of), and then a set amount moves into a stock market fund each month. This avoids putting all your money into the market at once, you get some interest on the money sitting in the liquid fund, and it gradually builds your stock market investments like a SIP.

For people with a lot of money to invest, STPs are a good way to reduce the risk of timing the market without completely leaving it. They follow a set of rules, which stops you from making emotional decisions when the market is volatile.

Match the horizon to the vehicle

The best type of investment depends on how long you have. If your goals are in 0-2 years, look at debt funds or Fixed Deposits. For a medium-term goal of 3-5 years, hybrid or index funds are a better fit. And for long-term goals (7-10 years or more) you could consider large, mid or small cap funds.

Your goals will change, so adjust how long you’ll invest as your milestones change. Saving for retirement needs a lot of patience; aiming for 20 years is in line with how the stock market usually performs. Generally, the longer you invest for, the less risk there is with stocks.

Before you invest anything, work out why you are investing. Buying a house, paying for your children’s education or saving for retirement each need a different level of risk. Balancing risk and the time you have to invest will make your plan more likely to succeed.

To make the first step easier, keep these action points in focus:

– Start with a small SIP to learn the process

– Prefer a simple index fund initially

– Avoid lump sum at the very beginning

– Increase contributions as confidence grows

Returns: what actually drives the gap

Will a SIP or a lump sum give better returns? It all depends on what’s happening in the market and how long you invest for. If you time a lump sum investment perfectly, it could make more than a SIP over a certain period. But if you get the timing wrong, a lump sum could do very badly.

SIPs usually give more steady and reasonable results over a long time because they spread out your investments. For people who want to build wealth slowly over many years, the consistency of a SIP is often more valuable than the chance of a quick profit from timing a lump sum.

What comes next for new investors

The practical steps are simple. Start investing as soon as you can, even with a small amount. Use SIPs to make sure you invest regularly. Choose a cheap index fund to make things simpler. Get used to how it all works for a few months, and then gradually increase how much you invest.

If you get a bit of extra money later on when the market is down, add it to your SIP. If you have a large lump sum, an STP could gradually move it into the stock market. And throughout all of this, have a long-term plan and don’t expect to get rich quickly.

The main point is this: for people starting out with 10,000 rupees in mutual funds, a SIP is a safer way to start than a lump sum. As you get more experience, you can combine the two. The aim isn’t to guess what the market will do, but to stay invested with a plan.