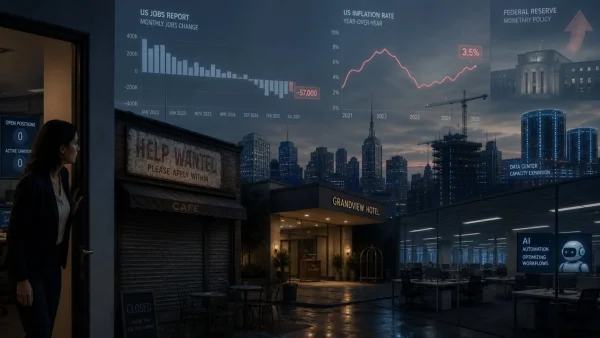

The numbers for June were a bit of a letdown. We saw 57,000 new jobs and an unemployment rate that inched to 4.2%. When you put that in the context of three-year high inflation and consumer sentiment near where it was right after the pandemic, you can see why people are asking questions about where we’re headed in the next few months.

It seems like firms are being more judicious with their headcount, if not putting a hard stop on it. The way officials put it, the 0.1% drop in the jobless rate from May has as much to do with fewer folks in the hunt for a job as it does with any upswing in openings.

Hiring cools as caution deepens

Fifty-seven thousand is a far cry from the kind of numbers we had last month. And when you factor in the downward revisions for April and May, the gains don’t look as robust as they did at first glance.

There were 7.1 million out of work, which is about the same as before. The change in the top-line number, for the most part, is a function of who is in the game, not a lot of new hiring.

Participation slips, masking labour slack

We’ve seen the labour force participation rate tick down 0.3 of a point to 61.5% – the lowest we’ve been in five years or more. That’s the reason the unemployment figure went down even though the hiring side of things was quiet.

If you look at prime-age workers, 25 to 54, their rate is at 83.3%, no better than it was in 2023. And long-term unemployment is still sitting at 1.9 million, accounting for over a quarter of those without a job.

Then there’s the structural side of it. With a wave of retirements and a lull in immigration, the pool of available workers isn’t really getting any bigger, so there’s a cap on how much you can hire even if the need is there.

Where jobs were gained and lost

It was a mixed bag by the numbers. Professional and business services put on 36,000, and social assistance 25,000, with a lot of that in family and individual services. Health care was up 22,000, but that’s not keeping up with its 12-month run of 38,000.

On the flip side, leisure and hospitality let go of 61,000, which is a little light for this time of year even with all the sporting events. The information sector is down again for the 17th time in 18 months; you can put that on the ongoing retooling in tech and the cost of AI.

Manufacturing and construction were up, and some would say it’s the data centre buildouts driving that. Financials didn’t move much, which is to be expected when the cost of money is what it is.

Wages and jobless claims show mixed signals

Earnings are up 3.5% on the year, and that’s enough to keep an eye on for anyone in charge of curbing inflation. As for the week’s jobless claims, they were flat, in line with a market that is softening but not in trouble.

Why expectations were missed

Some had a rosier view of June, with hopes for a strong showing from the government and the service industry. That didn’t happen. I think it comes down to a reluctance to commit and the fact that high prices are making people think twice about what they buy.

Put 57,000 in perspective with the 1,88,000 average and you’ll see the growth has been sapped, even if we haven’t hit a wall.

What it means for the Fed and growth

Things have been bumpy, but we’re not in freefall. The economy put up 2.1% in the opening quarter, though some see a lull in the second as financial conditions get tighter.

The Fed has made it known they are focused on price stability, and the market is already pricing in the possibility of a hike as early as now. How the rest of the data plays out will tell us what happens next.

Here is what the market is keying in on:

– Inflation running hot for three years

– A 3.5-3.75 percent federal funds rate

– Some talk of a hike this very month

– The 57,000 mark for June hiring

The bigger trend to watch

All told, we are moving from a very hot labor market to one that is just comfortable. Firms are holding back as they deal with the realities of AI, right-sizing in tech, and a return to normal in the service world.

Upcoming reports will make the path clearer. Should we see some steadiness in participation and a cool off in wages, the pressure for a harder line may ease. But if prices remain intransigent and hiring picks up, the risk of a rate move is back on the table. For the moment, the June figures are a call to be patient.