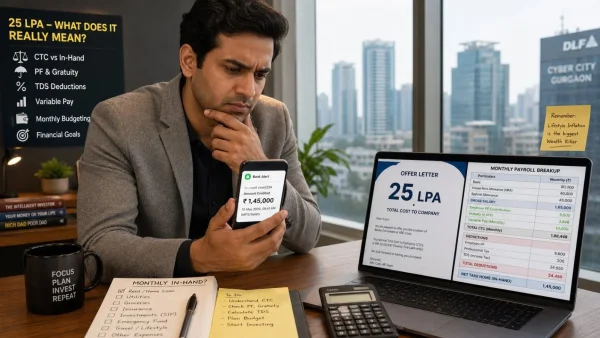

Then there is an IIT Roorkee alumnus whose post has some people re-reading their offer letters with a fine-tooth comb. On paper he was looking at a Rs 25 LPA deal, but the first time his salary hit his account it was for Rs 1,45,000. He’s been open about why that happens and how to be more realistic when you’re on the receiving end of an offer.

Who is behind the numbers and why they matter

Siddharth Maheshwari is 35, has an IIT Roorkee and ISB pedigree, and is an Associate Vice President with a Gurgaon startup. Out of ISB, he was handed an offer for Rs 25 lakh a year.

So when the notification for his first pay came in at Rs 1,45,000, he put it down to a bank mix-up at first. But it was no error on their part. It was the way the Cost to Company had been put together.

What your monthly payslip will tell you

On the surface, a Rs 25 LPA CTC is roughly Rs 2.08 lakh a month. But as Maheshwari puts it, the payroll is a bit starker than the figure suggests.

Run the numbers: you have a basic of Rs 80,000, HRA of 40k, 45k in special allowance and 5k for LTA and medical. Your gross comes in at about Rs 1.7 lakh.

But then come the obligatory deductions. Tally up an employee PF of some Rs 9,600, a professional tax of 200 and around 20k in TDS, and you are left with an in-hand of close to Rs 1.4 lakh.

The non-cash side of your CTC

Maheshwari points out that some of what is in your CTC is never going to be in your hand as cash. Some of it is for the long haul or is conditional.

Take the employer’s PF of Rs 9,600 a month, for instance. That is in your PF account and you can only get at it when you turn 58. You don’t get to the gratuity of Rs 3,200 a month until you’ve put in at least five years with the same employer and haven’t made an exit. Then there’s the medical insurance at Rs 2,500 a month – it’s a perk, but not something you can put in your pocket. As for the variable pay of Rs 12,500, that is more of a goal than a given; it hinges on how the company does and comes with no guarantees.

Where tax fits in

Maheshwari has crunched the figures for the new tax regime in FY 2026-27. Once you factor in the standard deduction and arrive at an annual taxable income of Rs 20.25 lakh, you are looking at a tax bill of some Rs 2.14 lakh for the year. Put that on a monthly basis and you have about Rs 18,000 in TDS. He puts that up against his previous rough figure of Rs 20,000 to make a point: how you structure things and which regime you pick will have a say in your cash flow.

What to keep in mind when you’re on the receiving end of an offer

If you ask Maheshwari, he has three points. One, don’t be swayed by the CTC numbers for PF and gratuity; they look good on paper but you can’t spend them. Two, handle variable pay with care because it isn’t fixed. And three, if you have a steep rent to cover, do your homework and see how the old and new tax regimes stack up.

His bottom line is to let in-hand be your guide. “Don’t just go by the CTC that looks nice in a brochure,” he says. “Get the number after tax and deductions. That’s what you use to pay your EMI and the landlord.”

Here is a quick way to run through an offer:

– Get the in-hand for the month, post-deductions

– When you budget, count variable as nothing

– Put the two tax regimes side by side

– Remember, PF and gratuity from the employer aren’t hard cash

The reason to pay attention

A big CTC can give you the wrong idea of where you stand, especially if you are just starting out. But your rent and savings are tied to what actually hits your account, not the total on the letterhead.

By breaking down a 25 LPA package into what you can really work with, his post is a good example to follow. In expensive cities, your HRA and tax decisions can make or break your take-home.

For the job hunter

There has been no shortage of talk around this kind of salary transparency. Even with comments turned off on the post, the word got out: do the math and be clear in your negotiations.

So if you are weighing a few offers, here is what to put to HR: the payroll set-up, the split between fixed and variable, the TDS you can expect, and the in-hand you will see. Because come June 15, 2026, or whenever your first pay comes in, those are the only figures that will count.