Even a small mistake with timing can slowly lower the amount of your savings from Section t80C. With the new tax rules (ITA 2025) now in effect, people who are still using the older tax system can definitely pay less tax, but they have to start planning ahead. The amount you can save is still the same, up to 1.5 lakh, and you can even go higher.

What changed with ITA 2025

From April of this year, Section 80C is referred to as Section 123 in the new ITA 2025. The benefit is the same as it always was, but more people aren’t eligible for it.

Only those who choose the older tax system can use this. The tax break is for individuals and Hindu Undivided Families, not for companies, partnerships or Limited Liability Partnerships.

Maximise the 1.5 lakh window

There are two advantages to this: you’ll pay less tax now, and your money will earn interest over time. This applies to all the investments you’re allowed to make, but how you do it is more important than wanting to do it.

If you invest early in the year, you get extra benefits you don’t even see. For example, if you put the full amount into a PPF (Public Provident Fund) by April 5th, you’ll get interest for the whole period including April. If you miss that, the interest only starts in May, and you lose a month’s worth.

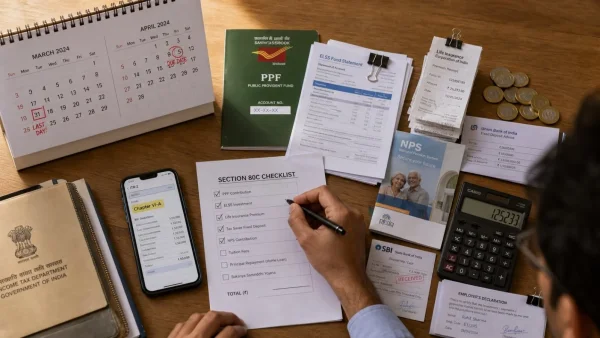

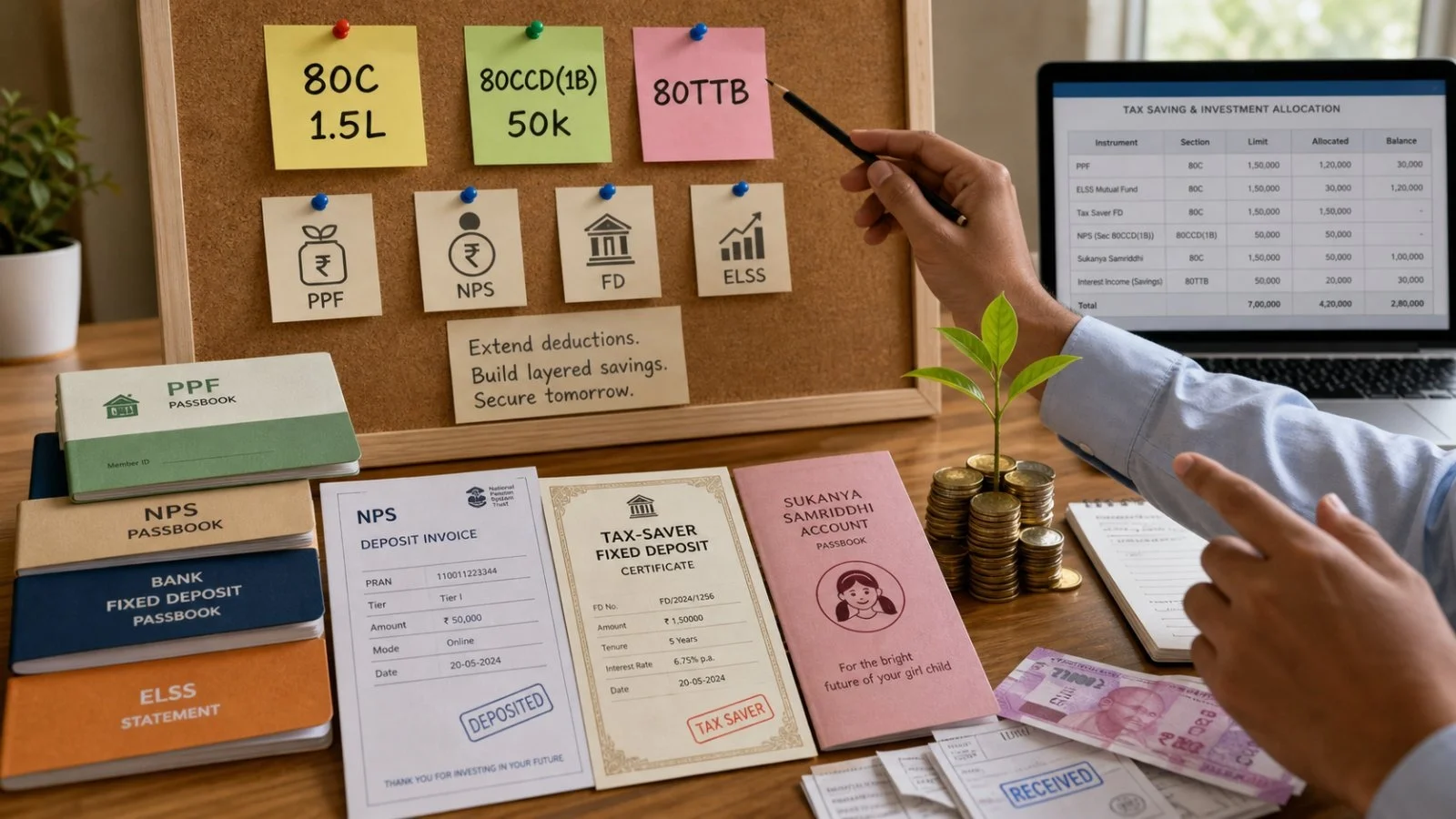

Using the entire 1.5 lakh is the best thing to do. You can put it all in one place, or spread it out. You could invest 50,000 in a PPF, 50,000 in ELSS (Equity Linked Savings Scheme), and pay 50,000 in life insurance, and get a variety of investments without losing any of the tax benefits.

Key moves investors should not miss:

– Complete eligible investments before 31 March

– Keep receipts, statements and premium proofs ready

– Decide old regime vs new regime early

– Avoid last-minute PPF deposits after 5 April

Extend deductions beyond 80C

There’s more room to save beyond that 1.5 lakh. You can get a further deduction of 50,000 under Section t80CCD(1B) by contributing to the National Pension Scheme. If you use this wisely, your total deductions can be 2 lakh in a year.

The law also mentions Section 80TTB for tax-saving fixed deposits (FDs). These options are in addition to the ones under Section 123 for those who are sticking with the old tax system.

Pick instruments by goal, not habit

The list of things you can invest in is long, but you should pick options that match your goals and how much risk you’re willing to take. Investments like ELSS and Unit Linked Insurance Plans that are tied to the market have the potential to grow more over many years.

If you are saving for retirement, Public Provident Fund, Employees Provident Fund, Senior Citizens Savings Scheme, National Pension Scheme and five-year tax-saving fixed deposits are generally safe. Parents might choose Sukanya Samriddhi Yojana and tuition fees for up to two children.

For general financial tidiness, paying the principal on a loan, paying premiums to the Life Insurance Corporation of India, registration and stamp duty, and National Savings Certificates all count. What you choose to include can change as your life changes, but you must have all the correct paperwork.

How to claim in your ITR

All the investments that will get you a deduction have to be finished by March 31st for that tax year. Have your deposit slips, bank statements, insurance receipt, account statements and NPS invoices available when you file your taxes.

You don’t have to tell your employer about these deductions. You can still claim them when you file your return, and your employer can change your TDS (Tax Deducted at Source) under the old system if you provide them with the details. In your tax return (ITR form) you’ll need to report these deductions under the section 'Deductions under Chapter VI-A‘.

Why this matters now

The more specific rules in ITA 12025 don’t reduce the amount of the deduction, but they do make it more expensive to delay. If you miss a contribution date or don’t use the full amount you’re allowed, you will get less tax relief now, and less interest on your money in the future.

The decision for the near future is simple: decide which tax system to use, carefully plan what to invest in, and invest as much as you can early on. The longer you put it off, the harder it will be to make up for it.

This information is just for guidance. Before you invest or file your taxes, it is a good idea to get advice from a qualified tax advisor.