A sharper grievance regime from the Reserve Bank of India is set to alter risk calculations across banks, NBFCs and fintechs. With RB-IOS, 2026 taking effect on July 1, 2026, compensation caps leap, timelines tighten, and uniform enforcement replaces geographic silos. For investors, this raises exposure to service failures but strengthens trust and dispute predictability.

Why this overhaul matters for investors

The most immediate change is financial exposure. Under the revamped Integrated Ombudsman Scheme, the Ombudsman can award up to Rs 30 lakh for consequential financial losses and up to Rs 3 lakh for time, expenses, harassment and mental anguish. Earlier limits stood at Rs 20 lakh and Rs 1 lakh.

That shift, combined with quicker, free-of-cost and non-adversarial resolution, could increase short-term compliance costs for regulated entities. Yet, the 'One Nation, One Ombudsman‘ approach promises consistency nationwide, reducing forum shopping and opaque outcomes, a positive for long-term customer confidence and brand equity.

Operationally, the scheme pushes lenders and payment players to tighten documentation, response discipline and internal redress systems. A centralised, uniform process will make gaps more visible, and the reputational fallout from poor service may now have clearer, costlier consequences.

Scope and eligibility under the new scheme

The scheme applies to a wide span of RBI-regulated entities. It covers banks, non-banking financial companies, prepaid payment instrument issuers, payment system participants, credit information companies, commercial banks, regional rural banks, scheduled and certain co-operative banks.

Complaints can be about deficiencies in service such as unauthorised transactions, digital payment failures, refund delays, credit report errors, and fee disputes. However, matters like loan sanction or pricing decisions, cases pending before courts, anonymous complaints, and issues raised without first approaching the entity are not maintainable.

The framework specifies detailed conditions to decide whether a complaint is maintainable. That precision helps consumers file correctly and signals regulated entities to address service gaps early, reducing escalation risk.

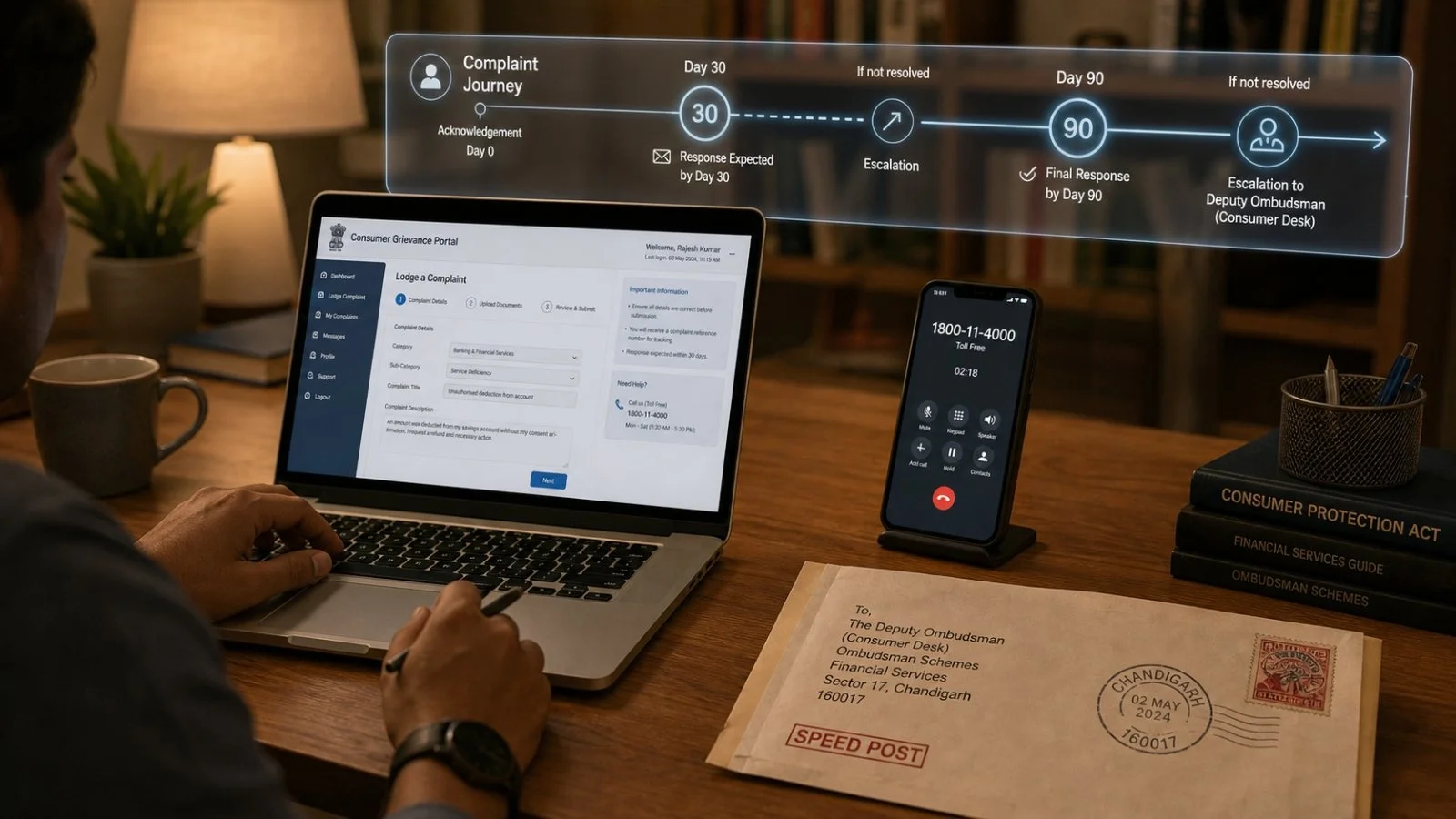

How the complaint journey works now

Consumers cannot approach the RBI Ombudsman first. They must file with the concerned regulated entity and wait up to 30 days, or a longer period if prescribed by RBI, NPCI or card network rules. If the response is unsatisfactory or the deadline lapses, they can approach the Ombudsman within 90 days.

Deputy Ombudsmen now carry expanded responsibilities. They can examine service deficiency complaints, facilitate settlements, reject non-maintainable cases, and close matters under specified provisions. The model remains simple and non-adversarial, allowing self-representation or authorised representatives.

For filing convenience, RBI has left multiple channels open. Customers can use the following options:

– The Complaint Management System portal

– Email submission to the RBI

– A physical application to the CRPC in Chandigarh

– Toll-free guidance on 14448 in multiple languages

Decisions, appeals and remedies

If a complaint is valid, the Ombudsman can direct the regulated entity to rectify the deficiency, perform specific obligations, refund money, pay compensation or take other remedial measures. There is no monetary limit on the value of disputes that can be brought before the Ombudsman.

Either party may appeal an Ombudsman award to the Appellate Authority within prescribed timelines. The Appellate Authority is the Executive Director in charge of RBI’s Consumer Education and Protection Department, or another officer of equivalent rank authorised by the Governor. Regulated entities cannot appeal if the award arose from their failure to furnish satisfactory and timely information or documents.

For investors, this appellate structure reduces uncertainty around prolonged litigation while preserving a check on awards. It also puts the onus on strong documentation and timely disclosures, making process discipline a competitive advantage.

Operational shifts to watch

A national, uniform process under 'One Nation, One Ombudsman‘ breaks the link between case handling and geography. Complaints are processed without regard to where the customer or the entity is located, creating a single standard for grievance redressal.

RBI has also centralised intake and processing to speed up resolution and improve transparency. A centralised receipt and processing centre in Chandigarh, combined with the CMS portal and helpline support, makes the journey simpler for consumers and easier to audit for regulators.

Key implications for compliance and service teams include:

– Faster clocks, stricter maintainability screening

– Higher award exposure for proven service gaps

– More emphasis on early settlement and documentation

– Increased oversight through centralised processing

Transition and what comes next

RB-IOS, 2026 replaces the 2021 framework, but there is a clean handover for ongoing cases. Complaints and appeals already filed under the 2021 scheme will continue under the earlier framework, avoiding disruption or mid-course changes for those matters.

To guide both entities and customers, RBI has published an FAQ explaining the provisions and operational aspects. The regulator says the objective is faster, cost-free and non-adversarial redressal that strengthens accountability.

For investors, the near-term watchlist is clear. Track complaint volumes, turnaround times and award trends. Look for investments in complaint management systems, staff training and data quality. Entities that adapt quickly should benefit from lower dispute friction and improved trust, while laggards face rising costs and reputational drag.